# install.packages("pacman") # first time only

library("pacman")

pacman::p_load_gh("wesland/auditanalytics")

pacman::p_load(tidyverse, plotluck, kableExtra, ggthemes, Hmisc, psych)Audit Analytics

分析環境を作る。

RとRstudioをインストールする。

- Install R

- Install RStudio (or VS Code)

- Install Quarto

パッケージをインストール

最初にinstall.packages("pacman")でpacmanパッケージをインストールし, library(pacman)で読み込みます。

次に,pacmanパッケージのp_load_gh()関数を使ってGitHubからauditanalyticsパッケージをインストール・読み込みを行い, p_load()関数でCRANから必要なパッケージをインストール・読み込みを行います。

Rの入門

- Assign a value to a variable with

<-or=. - An object’s name is flexible, but it must begin with a letter and typically follows snake_case.

- like

df_original,my_data,total_asset, etc.

- like

- Use

#for comments.

Assigning values

Replace the right-hand side with the left-hand side object x with <- or =.

<-

x <- 3

4 -> y

x[1] 3y[1] 4Example

pipe operator %>% or |>

Use pipes %>% or |> to chain functions together. The pipe operator assigns the left-hand side result to the first argument of the right-hand side function.

A |> function(B)

has same meaning as function(A, B).

Example

Try the following code.

x <- 1:100 # assign 1 to 100 to x

# calculate the sum of x above 50

# nested

sum(subset(x, x > 50))[1] 3775# use standard pipe

x |> subset(x > 50) |> sum()[1] 3775# use magrittr pipe

x %>% subset(x > 50) %>% sum[1] 3775Use packages

We can use packages to add functionality beyond the functions that come with R. Install a package to use it.

install.packages("pacman")read csv data

industry_stats <- readr::read_csv( # read csv file

system.file("extdata", # file path

"ch_2_dataset.csv", # file name

package = "auditanalytics", # package name

mustWork = TRUE # error if file not found

)

)

head(industry_stats) # show the first 3 rows# A tibble: 6 × 6

ticker employees income sales capitalization fiscal_year

<chr> <dbl> <dbl> <dbl> <dbl> <dbl>

1 GE 319 20829 160854 382421 2006

2 GE 319 20829 160854 382421 2006

3 GE 327 22208 169719 370240 2007

4 GE 327 22208 169719 370240 2007

5 GE 316 16711 148559 367474 2005

6 GE 316 16711 148559 367474 2005Chapter 2: Foundations of Audit Analytics

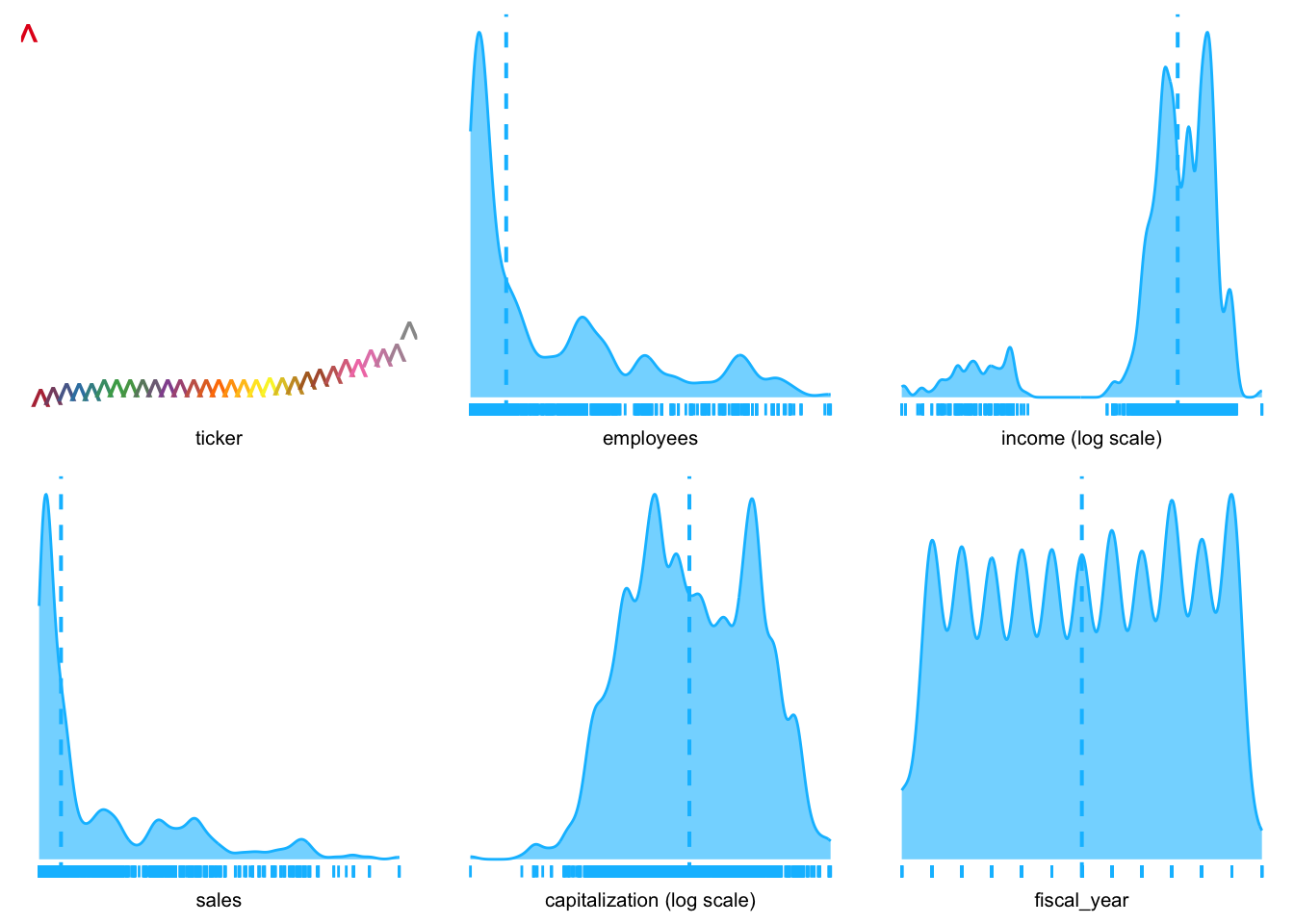

plotluck packages

plotluck(industry_stats, .~1)

.~1 shows distribution of each variable in the data frame, separately.

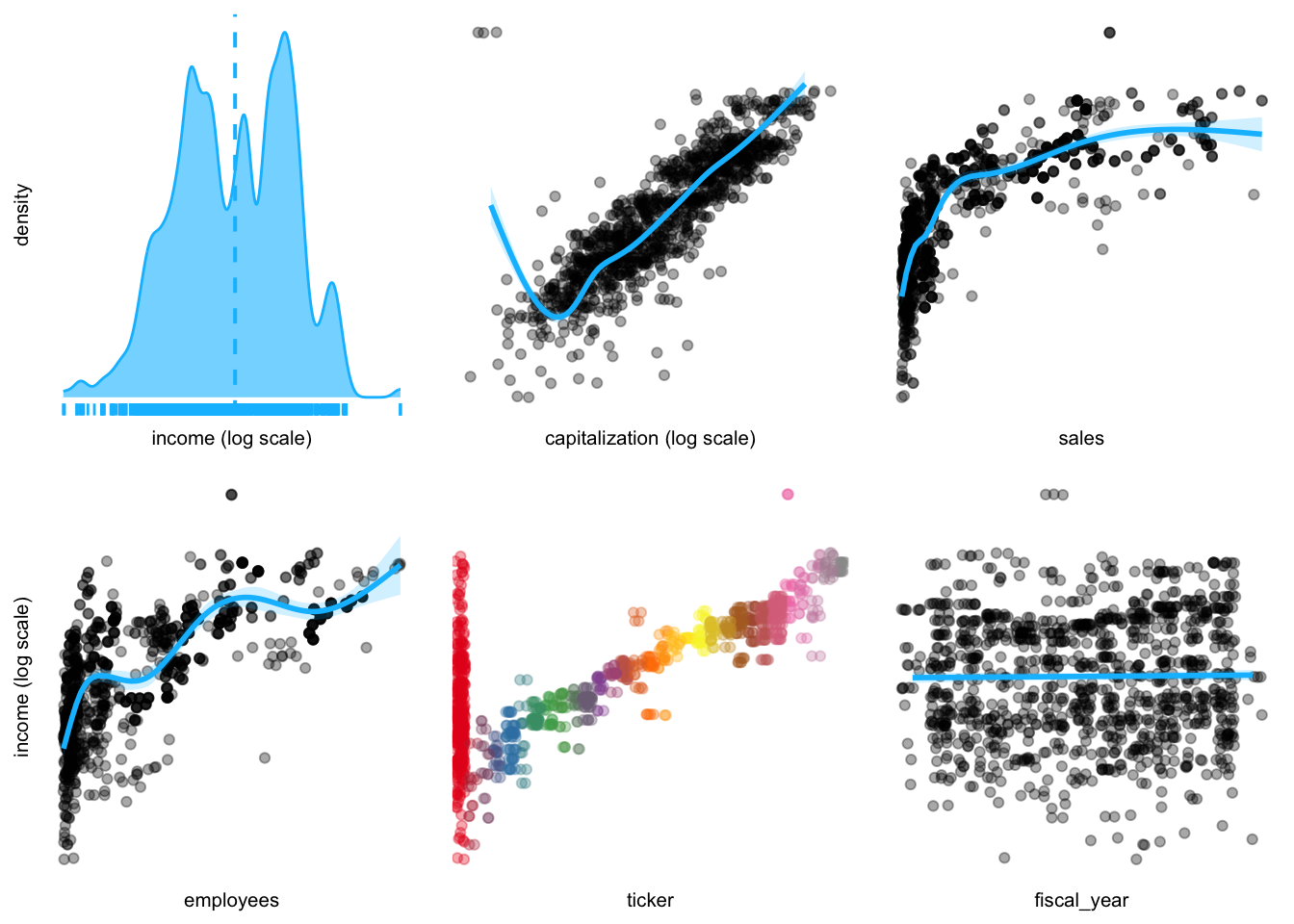

industry_stats |>

dplyr::filter(income >= 0 ) |> # filter data

plotluck(income ~ .) # plot the data

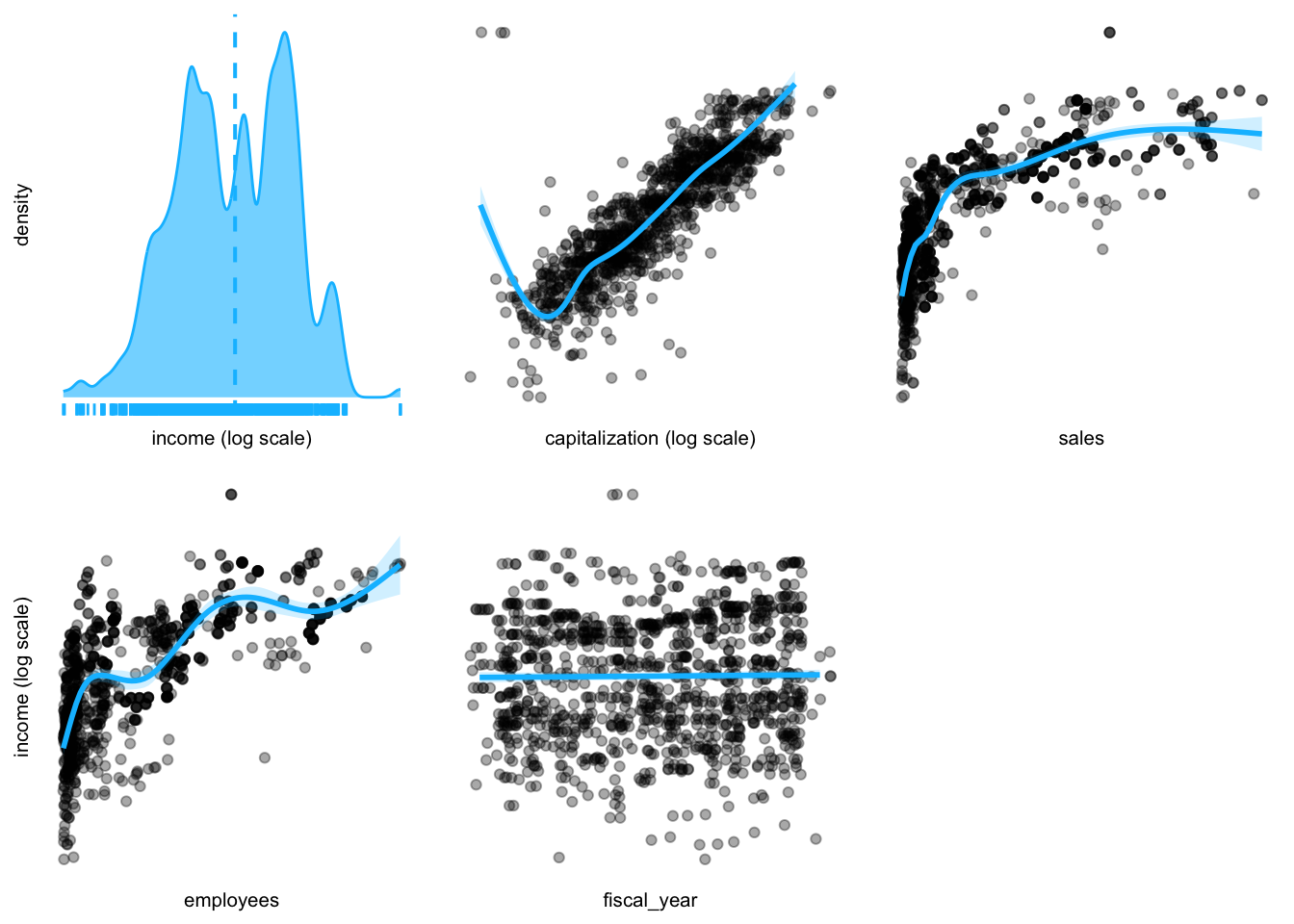

industry_stats |>

dplyr::select(-ticker) |> # tickerを除外

dplyr::filter(income >= 0) |> # 利益が0以上のデータ

plotluck(income ~ .) # 作図

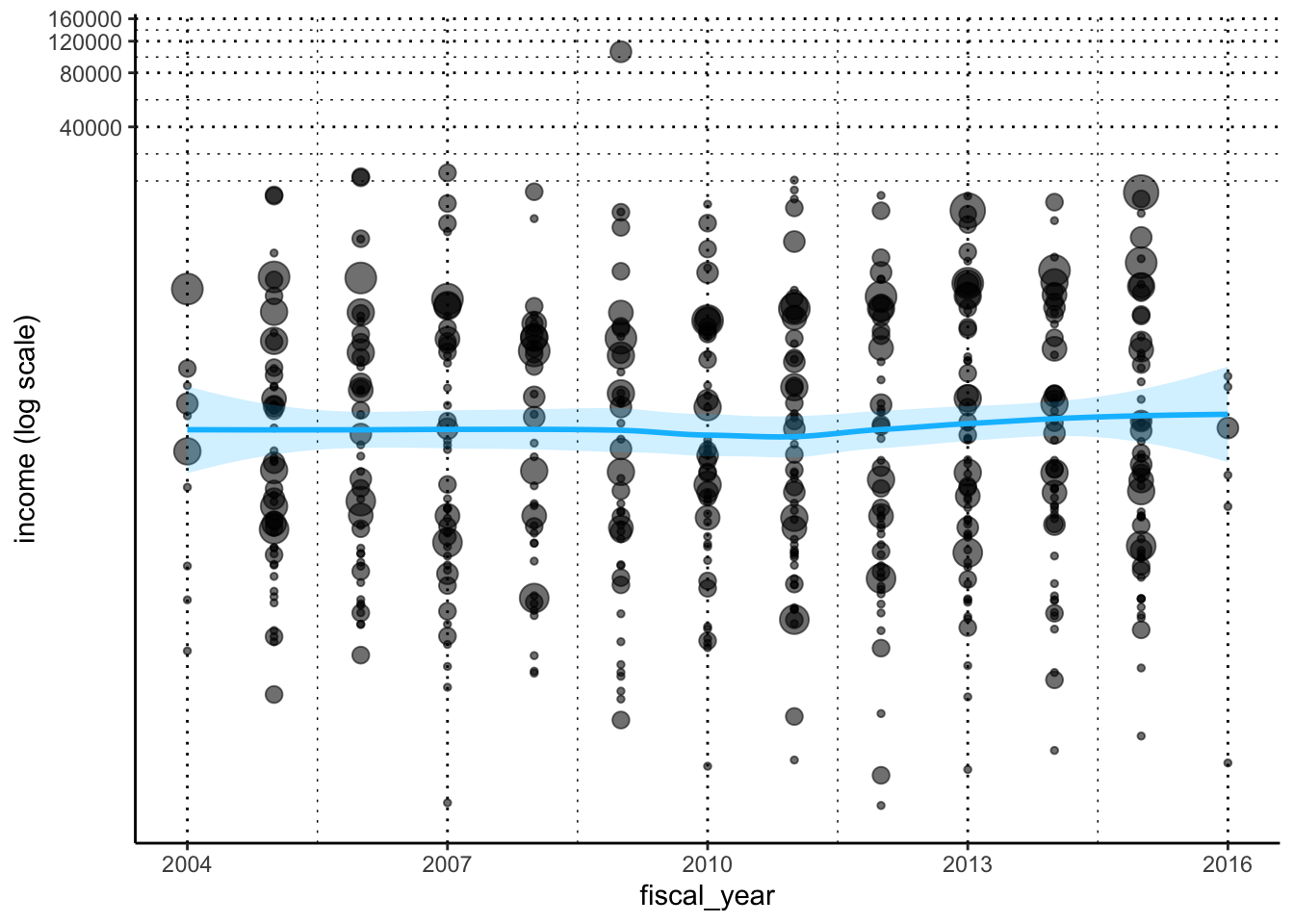

industry_stats |>

dplyr::filter(income >= 0) |> # 利益が0以上のデータ

plotluck(income ~ fiscal_year) # income vs fiscal year

sox_stats <- read_csv( # read csv file

system.file(

"extdata",

"ch_2_data_types.csv", # dataset

package = "auditanalytics",

mustWork = TRUE

)

)

head(sox_stats)# A tibble: 6 × 19

ticker date card disc hack insd phys port stat unkn effective_303

<chr> <dbl> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 A 2008 0 0 0 0 0 1 0 0 1

2 A 2008 0 0 0 0 0 1 0 0 1

3 A 2008 0 0 0 0 0 1 0 0 1

4 A 2008 0 0 0 0 0 1 0 0 1

5 A 2008 0 0 0 0 0 1 0 0 1

6 AAN 2011 0 0 0 0 0 0 1 0 1

# ℹ 8 more variables: mat_weak_303 <dbl>, sig_def_303 <dbl>, auto_1 <dbl>,

# auditor_agrees_303 <dbl>, effective_404 <dbl>, audit_fee <dbl>,

# non_audit_fee <dbl>, tax_fees <dbl>summary(sox_stats) # descriptive stats ticker date card disc

Length:1514 Min. :2005 Length:1514 Min. :0.0000

Class :character 1st Qu.:2007 Class :character 1st Qu.:0.0000

Mode :character Median :2010 Mode :character Median :0.0000

Mean :2010 Mean :0.1739

3rd Qu.:2013 3rd Qu.:0.0000

Max. :2016 Max. :1.0000

NA's :2 NA's :2

hack insd phys port

Min. :0.0000 Min. :0.0000 Min. :0.0000 Min. :0.0000

1st Qu.:0.0000 1st Qu.:0.0000 1st Qu.:0.0000 1st Qu.:0.0000

Median :0.0000 Median :0.0000 Median :0.0000 Median :0.0000

Mean :0.2467 Mean :0.1382 Mean :0.0463 Mean :0.2837

3rd Qu.:0.0000 3rd Qu.:0.0000 3rd Qu.:0.0000 3rd Qu.:1.0000

Max. :1.0000 Max. :1.0000 Max. :1.0000 Max. :1.0000

NA's :2 NA's :2 NA's :2 NA's :2

stat unkn effective_303 mat_weak_303

Min. :0.00000 Min. :0.00000 Min. :0.0000 Min. :0.00000

1st Qu.:0.00000 1st Qu.:0.00000 1st Qu.:1.0000 1st Qu.:0.00000

Median :0.00000 Median :0.00000 Median :1.0000 Median :0.00000

Mean :0.03704 Mean :0.03968 Mean :0.9616 Mean :0.03241

3rd Qu.:0.00000 3rd Qu.:0.00000 3rd Qu.:1.0000 3rd Qu.:0.00000

Max. :1.00000 Max. :1.00000 Max. :1.0000 Max. :1.00000

NA's :2 NA's :2 NA's :2 NA's :2

sig_def_303 auto_1 auditor_agrees_303 effective_404

Min. :0.0000 Min. :0.0000 Min. :0.00000 Min. :0.0000

1st Qu.:0.0000 1st Qu.:0.0000 1st Qu.:0.00000 1st Qu.:0.0000

Median :0.0000 Median :0.0000 Median :0.00000 Median :0.0000

Mean :0.1157 Mean :0.2037 Mean :0.08003 Mean :0.3935

3rd Qu.:0.0000 3rd Qu.:0.0000 3rd Qu.:0.00000 3rd Qu.:1.0000

Max. :1.0000 Max. :1.0000 Max. :1.00000 Max. :1.0000

NA's :2 NA's :2 NA's :2 NA's :2

audit_fee non_audit_fee tax_fees

Min. : 100000 Min. : 0 Min. : 0

1st Qu.: 3785984 1st Qu.: 477686 1st Qu.: 93140

Median : 7956000 Median : 1068000 Median : 370000

Mean : 15321536 Mean : 3679039 Mean : 1451705

3rd Qu.: 17800000 3rd Qu.: 3400000 3rd Qu.: 1311000

Max. :112200000 Max. :41100000 Max. :20800000

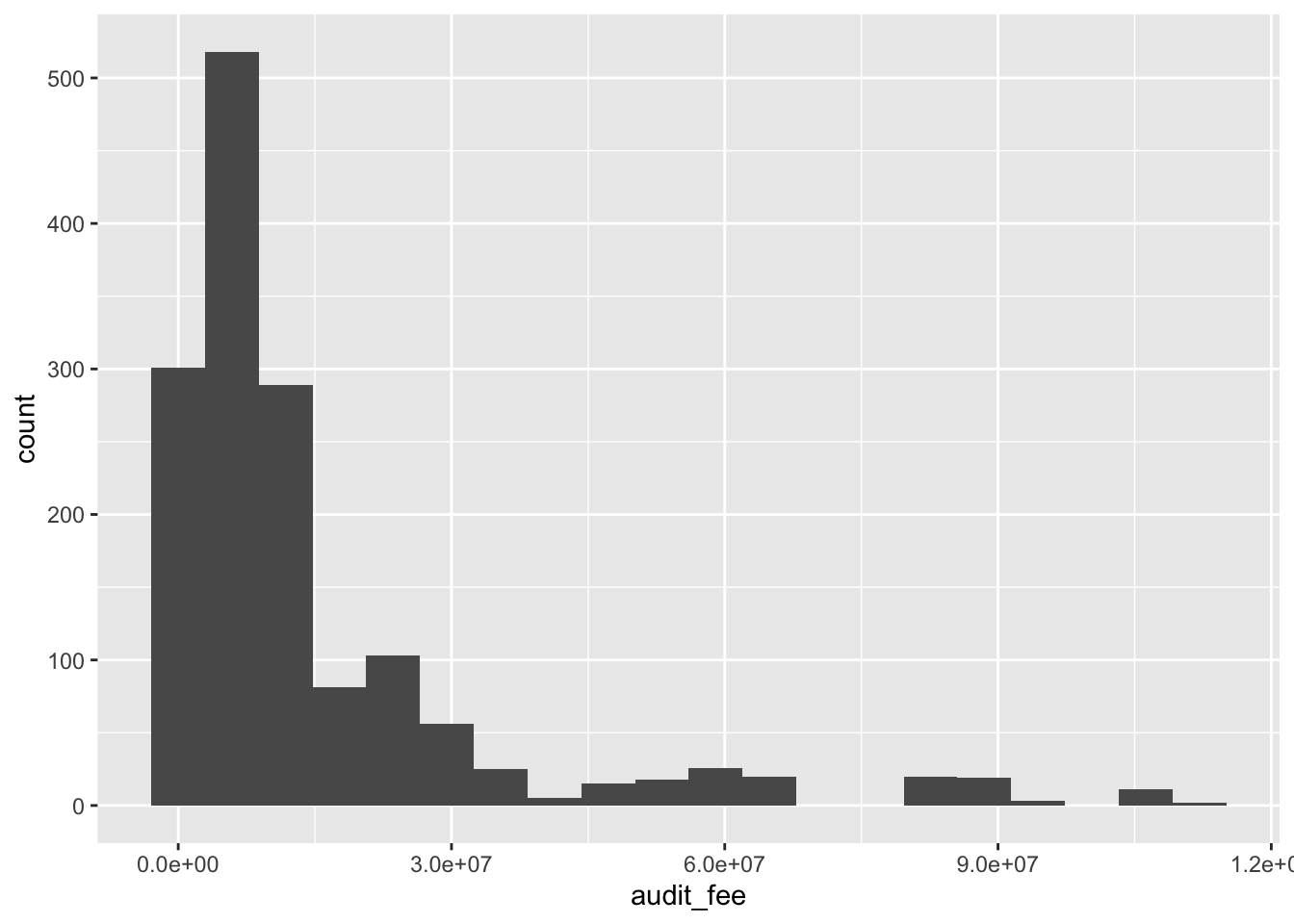

NA's :2 NA's :2 NA's :2 make histogram

sox_stats |> # choose the variables

ggplot() + # プラスの直後で改行OK

aes(x = audit_fee) + # 変数を指定

geom_histogram(bins = 20) # ヒストグラム

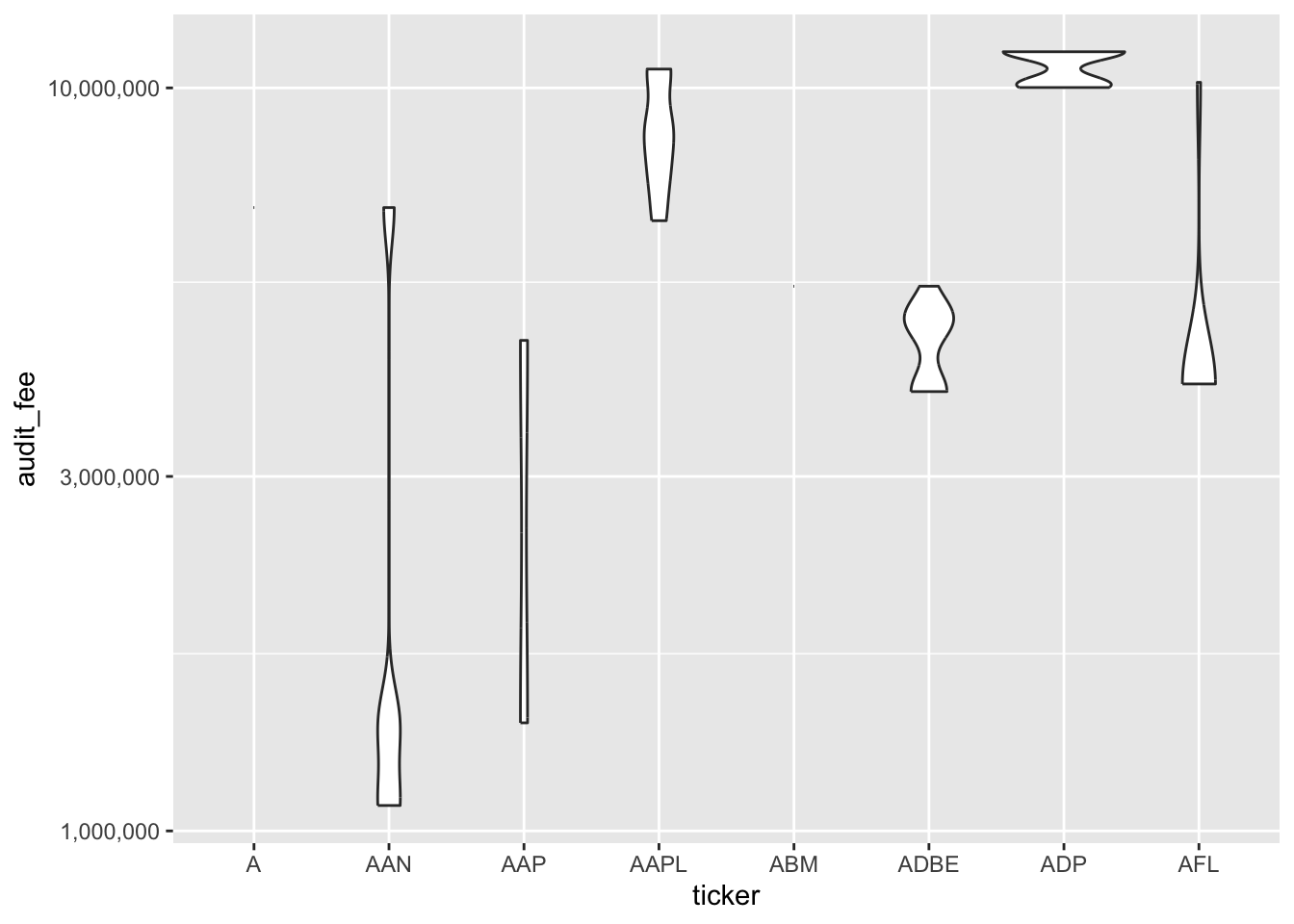

Categorical Data

sox_stats |>

filter(as.character(ticker) < "AI") |> # data before "AI"

ggplot() +

aes(x = ticker, y = audit_fee) + # 軸の指定

geom_violin() + # violin plot

scale_y_continuous(

trans = "log10", # 常用対数

labels = scales::comma # comma format

)

bank_fin <- read_csv( # CSVファイルを読み込む

system.file(

"extdata",

"ch_2_yahoo_fin.csv", # データセット

package = "auditanalytics",

mustWork = TRUE

)

)

head(bank_fin)# A tibble: 6 × 9

ticker name price change percent_change volume vol_ave capitalization

<chr> <chr> <dbl> <chr> <dbl> <dbl> <dbl> <chr>

1 HSBC-PA HSBC Holdi… 2.65e1 0.00 0 2.64e4 6.15e4 541.154B

2 BRK-B Berkshire … 2.01e2 1.92 0.97 2.02e6 3.78e6 493.498B

3 BRK-A Berkshire … 3.02e5 2631.… 0.88 2.43e2 2.45e2 492.962B

4 V Visa Inc. 1.80e2 -0.87 -0.48 3.59e6 6.91e6 403.496B

5 JPM JPMorgan C… 1.09e2 1.10 1.02 6.51e6 1.15e7 347.679B

6 SAN-PB Banco Sant… 2.27e1 0.04 0.18 1.20e4 1.94e4 349.445B

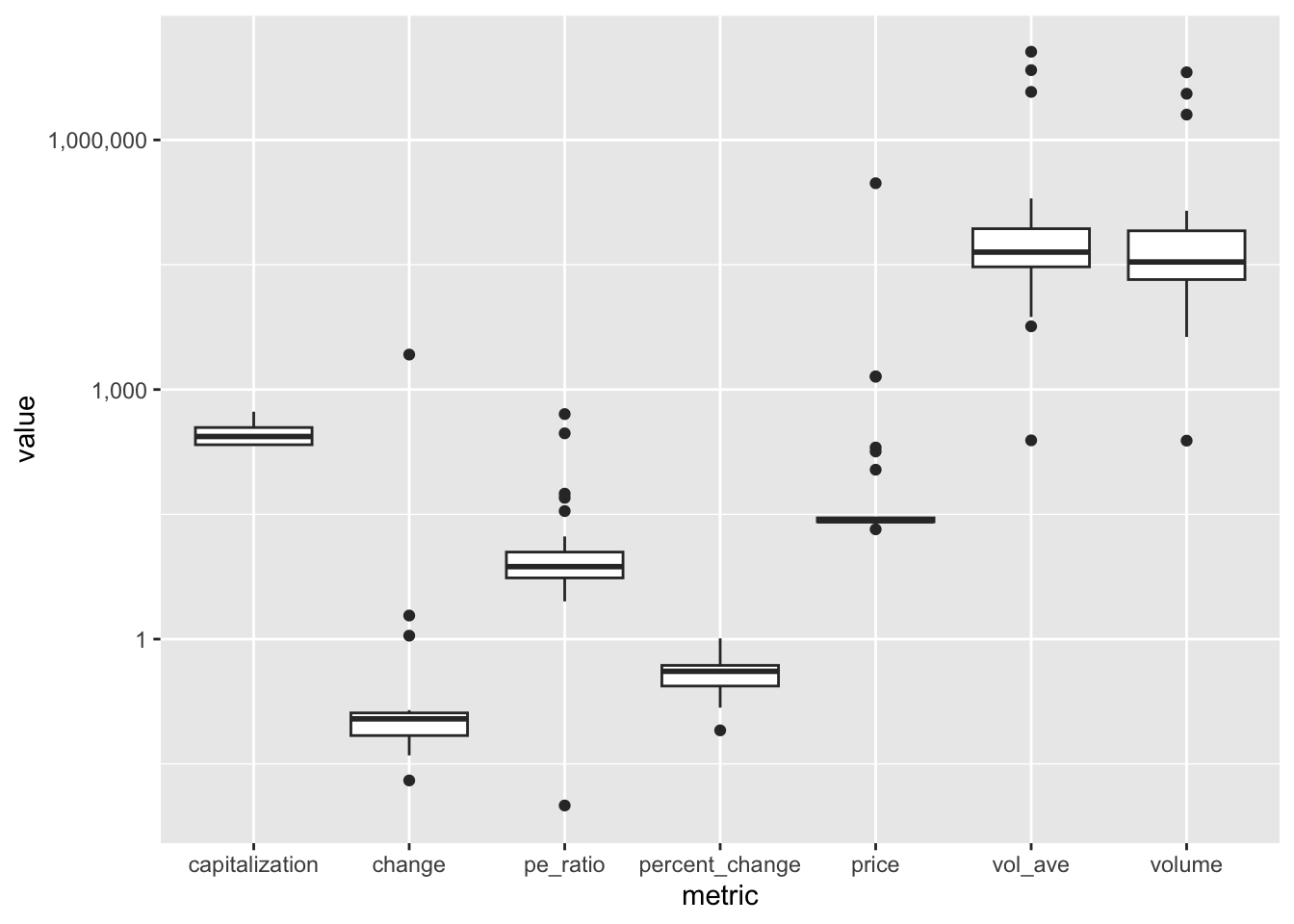

# ℹ 1 more variable: pe_ratio <dbl>bank_fin |>

filter(change != "ticker") |> # ticker以外

mutate(# データの変換

change = as.numeric(change), # 数値に変換

capitalization = as.numeric( # Bを削除

str_replace(capitalization, "B", "")

)

) |>

pivot_longer( # wide to long

cols = c(price, change, percent_change, volume,

vol_ave, capitalization, pe_ratio),

names_to = "metric", # 変数名

values_to = "value" # 値

) |>

ggplot() + # 作図

aes(x = metric, y = value) + # 軸の指定

geom_boxplot() + # 箱ひげ図

scale_y_continuous(

trans = "log10",

labels = scales::comma

) # 縦軸を対数

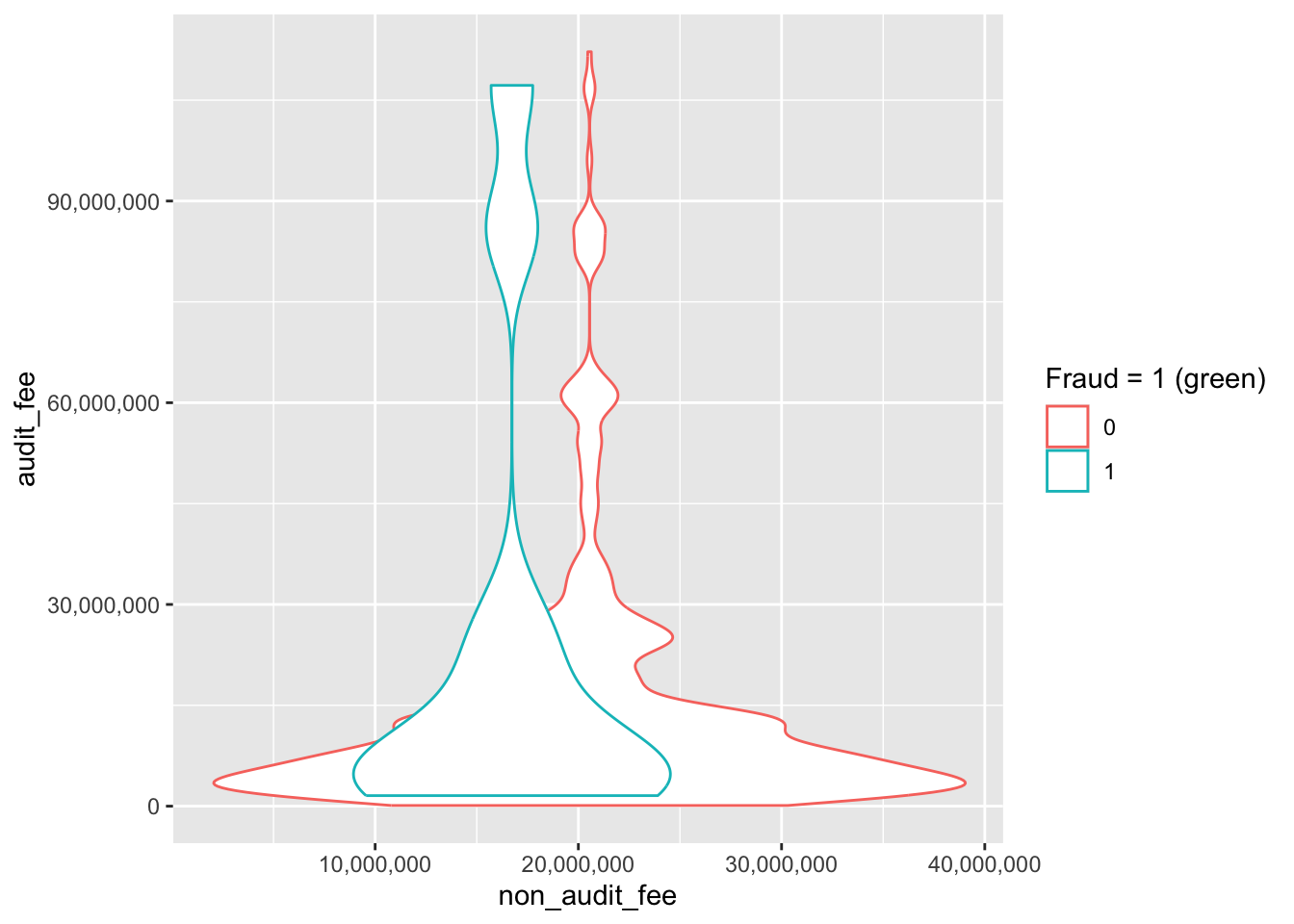

Binary Data

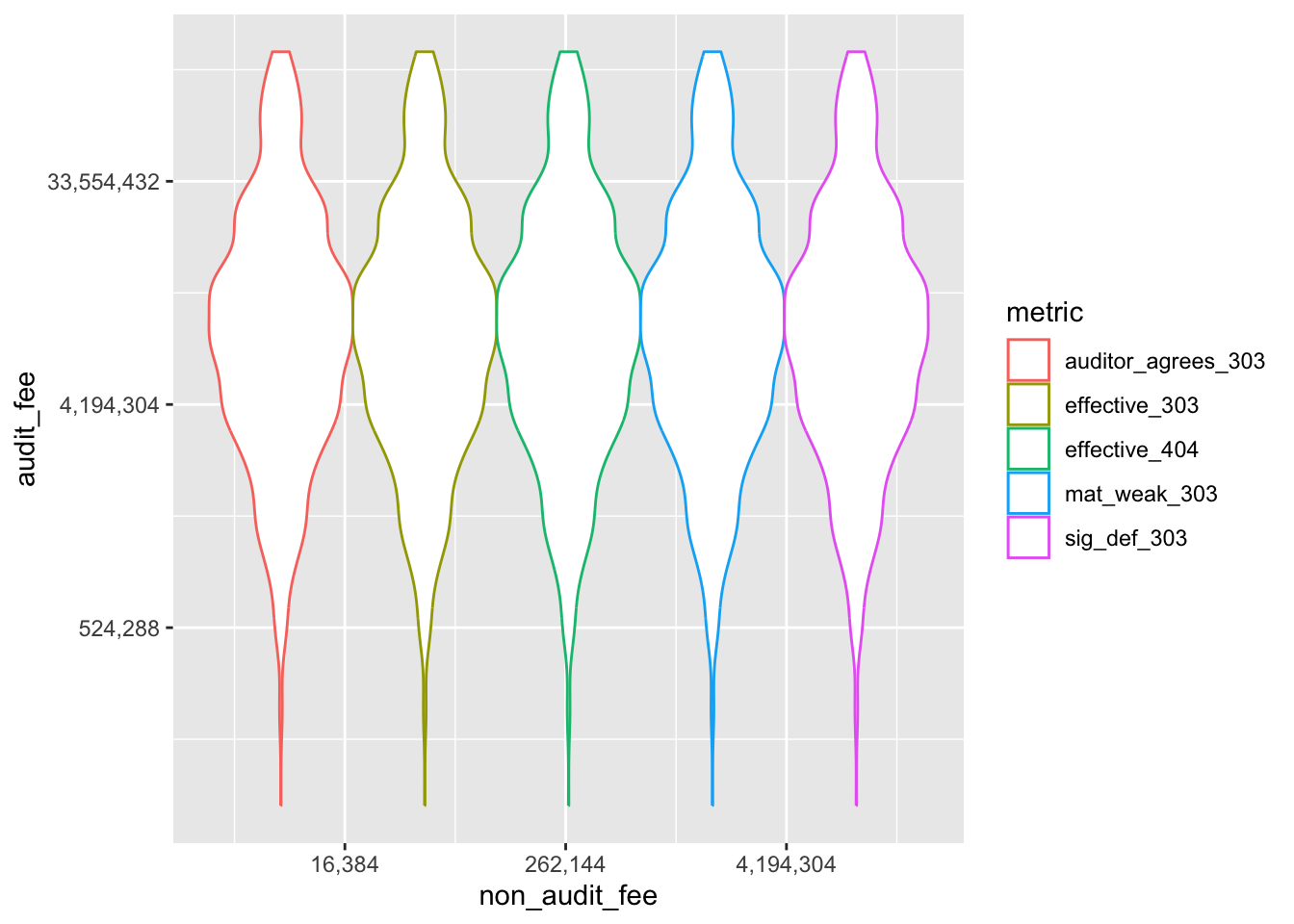

ggplot(sox_stats) +

aes(x = non_audit_fee, y = audit_fee, col = card) + # 軸と色分け

geom_violin() + # ヴァイオリンプロット

labs(col = "Fraud = 1 (green)") + # 軸ラベル

scale_y_continuous(labels = scales::comma) +

scale_x_continuous(labels = scales::comma)

整数に変換 as.integer()

sox_stats$card <- as.integer(sox_stats$card)

sox_stats_long <- sox_stats |>

pivot_longer( # wide to long

cols = c(effective_303, mat_weak_303, sig_def_303,

effective_404, auditor_agrees_303),

names_to = "metric", # 変数名

values_to = "value") # 値

# 作図

ggplot(sox_stats_long) +

aes(x = non_audit_fee, y = audit_fee, col = metric) +

geom_violin() + # バイオリン・プロット

scale_x_continuous(trans = "log2", labels = scales::comma) +

scale_y_continuous(trans = "log2", labels = scales::comma) # 対数軸

Make an original function

rdate <- function( # 引数を指定

x,

min = paste0(format(Sys.Date(), "%Y"), "-01-01"),

max = paste0(format(Sys.Date(), "%Y"), "-12-31"),

sort = TRUE

) { # 関数の本体

dates <- sample(

seq(as.Date(min), as.Date(max), by = "day"),

x, replace = TRUE)

if (sort == TRUE) {

return(sort(dates))

} else {

return(dates)

}

}

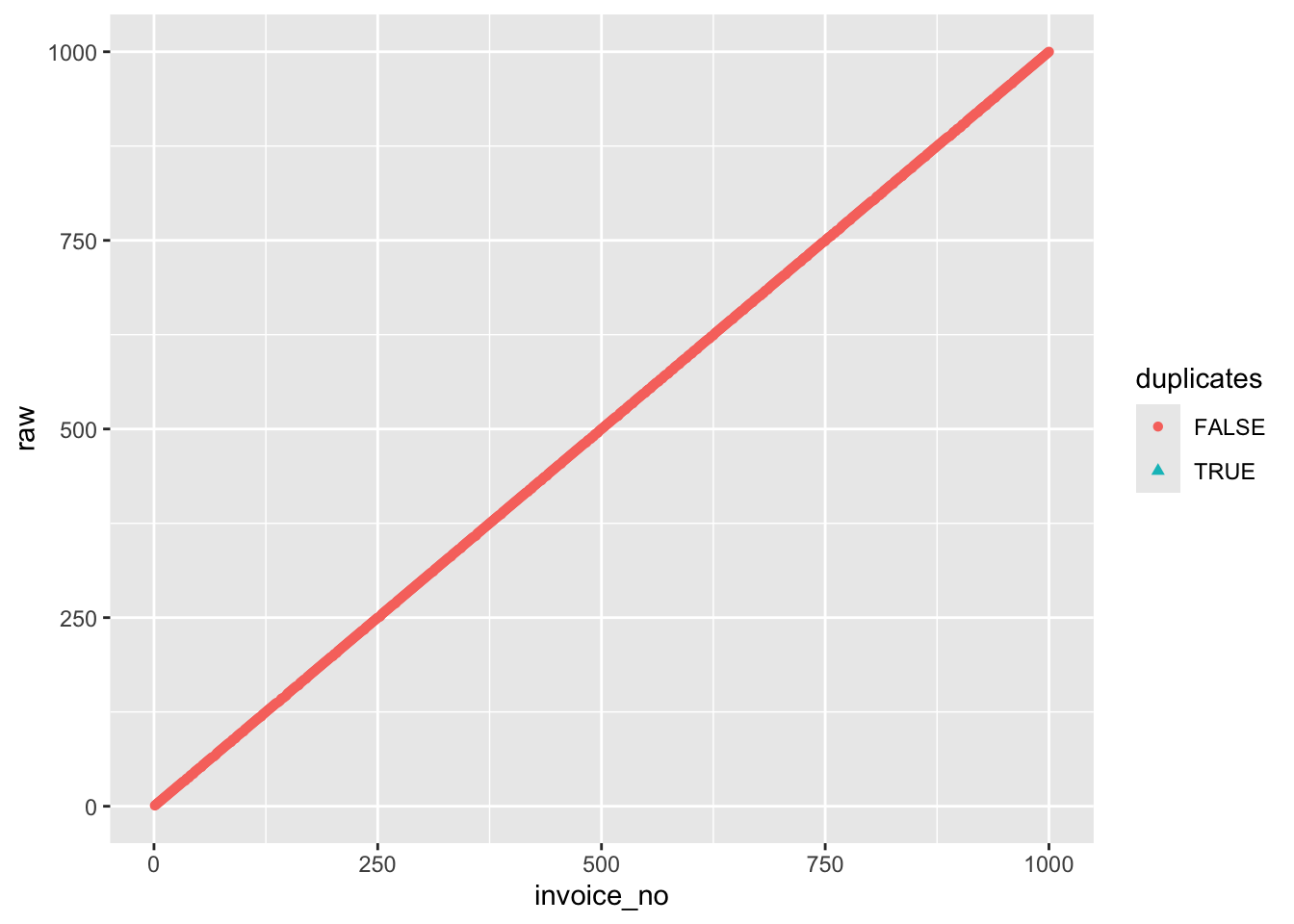

journal_ent_no <- tibble( # data.frameを作成

date = rdate(1000), # ランダムな日付

invoice_no = seq(1, 1000) + rbinom(1000, 1, 0.1) # 請求書番号

) |>

arrange(date) |> # 日付で並び替え

mutate( # 重複する日付をマーク

invoice_no = if_else(duplicated(invoice_no), NA, invoice_no),

duplicates = duplicated(invoice_no) # duplicates

)

journal_dups <- journal_ent_no |>

mutate(

raw = row_number(), # row number

duplicates = duplicated(invoice_no) # duplicates

)

glimpse(journal_dups)Rows: 1,000

Columns: 4

$ date <date> 2024-01-01, 2024-01-01, 2024-01-01, 2024-01-01, 2024-01-02…

$ invoice_no <int> 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, …

$ duplicates <lgl> FALSE, FALSE, FALSE, FALSE, FALSE, FALSE, FALSE, FALSE, FAL…

$ raw <int> 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, …table(journal_dups$duplicates)

FALSE TRUE

919 81 ggplot(journal_dups) +

aes(x = invoice_no, y = raw,

shape = duplicates, color = duplicates) +

geom_point() # 散布図

journal_ent_no |>

filter(duplicates == TRUE, invoice_no < 100) |>

kable(longtable = T, caption = "Duplicated Invoices") |>

kable_styling(

bootstrap_options = c("striped", "hover", "condensed"),

full_width = F, font_size = 20)| date | invoice_no | duplicates |

|---|---|---|

| NA | NA | NA |

| :---- | ----------: | :---------- |

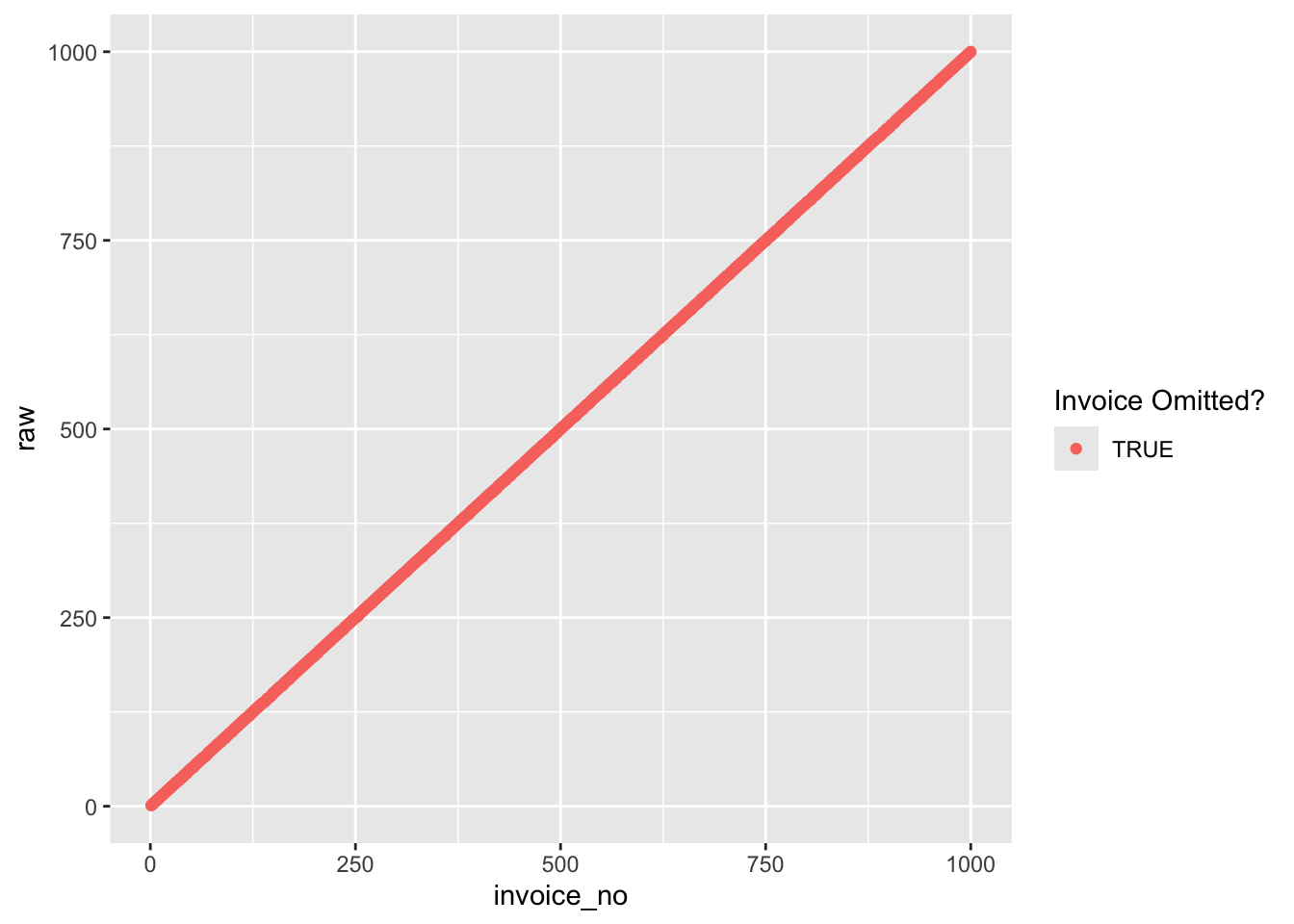

journal_dups <- journal_dups |>

mutate(

invoice = journal_ent_no$invoice_no,

omit = !raw %in% journal_ent_no$invoice

)

glimpse(journal_dups)Rows: 1,000

Columns: 6

$ date <date> 2024-01-01, 2024-01-01, 2024-01-01, 2024-01-01, 2024-01-02…

$ invoice_no <int> 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, …

$ duplicates <lgl> FALSE, FALSE, FALSE, FALSE, FALSE, FALSE, FALSE, FALSE, FAL…

$ raw <int> 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, …

$ invoice <int> 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, …

$ omit <lgl> TRUE, TRUE, TRUE, TRUE, TRUE, TRUE, TRUE, TRUE, TRUE, TRUE,…ggplot(journal_dups) +

aes(x = invoice_no, y = raw, col = omit) +

geom_point() + labs(col = "Invoice Omitted?")

Big Data

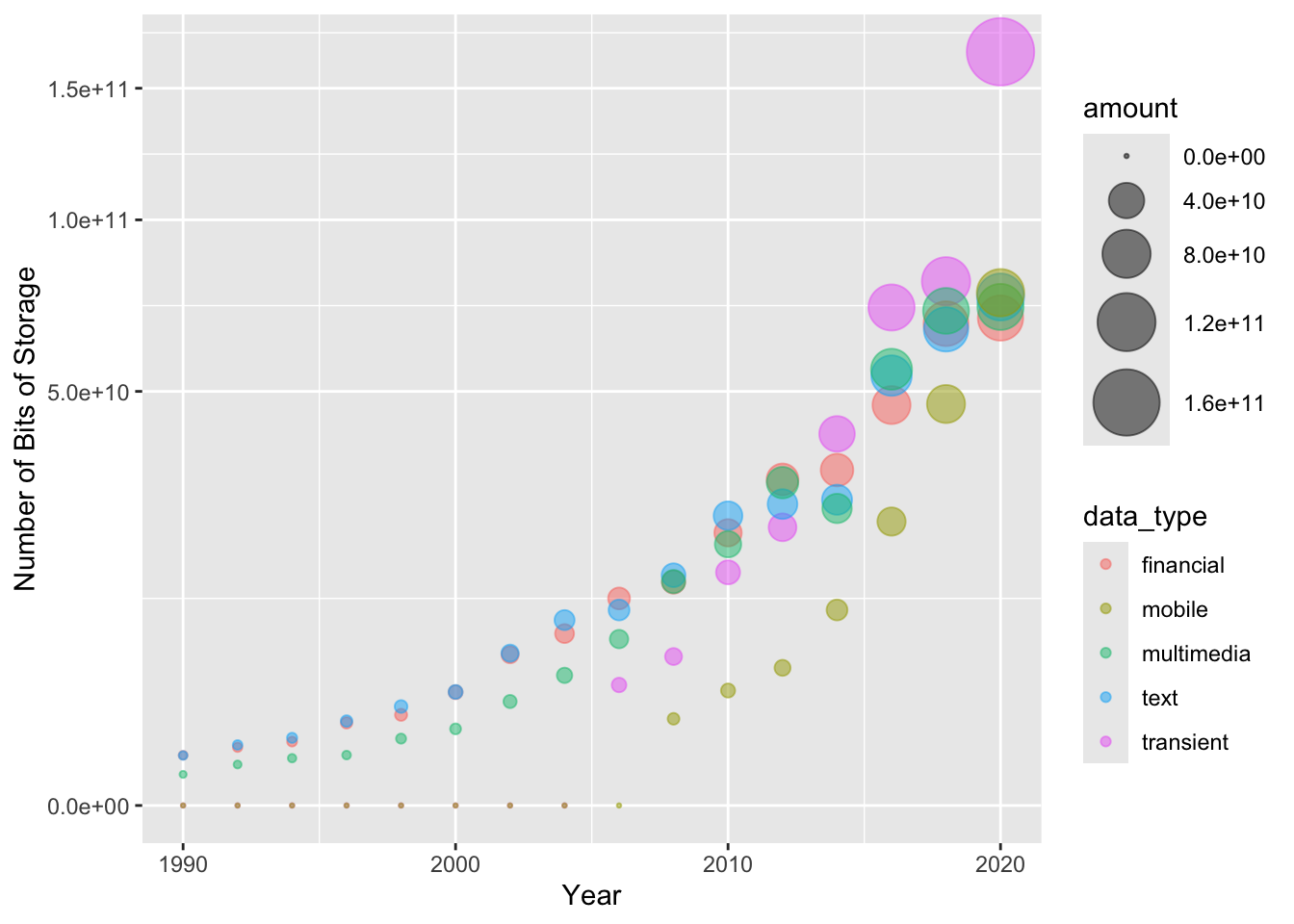

big_data <- read_csv(

system.file(

"extdata",

"ch1_amount_data.csv",

package = "auditanalytics",

mustWork = TRUE

)

) |>

pivot_longer(# wide to long

cols = c(-year),

names_to = "data_type",

values_to = "value"

)

head(big_data)# A tibble: 6 × 3

year data_type value

<dbl> <chr> <dbl>

1 1930 transient 0

2 1930 financial 323436613.

3 1930 text 332755554.

4 1930 multimedia 0

5 1930 mobile 0

6 1932 transient 0 big_data$amount <- sqrt(big_data$value)

big_data %>%

ggplot() + aes(x = year, y = amount, col=data_type) +

geom_point(aes(color = data_type, size = amount), alpha = 0.5) +

scale_size(range = c(0.5, 12)) +

scale_y_continuous(trans = "sqrt") +

xlim(1990,2020) + xlab("Year") +

ylab("Number of Bits of Storage")

Vectors

a <- c(1, 2, 5.3, 6, -2, 4) # number vector

b <- c("one", "two", "three") # character vector

c <- c(TRUE,TRUE,TRUE,FALSE,TRUE,FALSE) # logical vector

a[c(2,4)] # 2nd and 4th elements of the vector[1] 2 6Matrix

sequence of numbers from 1 to 25

vector <- seq(1, 25)

r <- 5

c <- 5

mat <- matrix(vector,

nrow = r, # row

ncol = c, # column

byrow = FALSE # 行と列を入れ替えない

)

print(mat) # 行列を表示 [,1] [,2] [,3] [,4] [,5]

[1,] 1 6 11 16 21

[2,] 2 7 12 17 22

[3,] 3 8 13 18 23

[4,] 4 9 14 19 24

[5,] 5 10 15 20 25Try this code

Indexing

# 5行4列の行列を作成

y <- matrix(1:20, nrow=5,ncol=4)

y [,1] [,2] [,3] [,4]

[1,] 1 6 11 16

[2,] 2 7 12 17

[3,] 3 8 13 18

[4,] 4 9 14 19

[5,] 5 10 15 20# another example

cells <- c(1,26,24,68)

rnames <- c("R1", "R2")

cnames <- c("C1", "C2")

mymatrix <- matrix(cells,

nrow = 2,

ncol = 2,

byrow = TRUE,

dimnames = list(rnames, cnames)

)

mymatrix C1 C2

R1 1 26

R2 24 68mat[, 4] # 4th column of the matrix[1] 16 17 18 19 20mat[3,] # 3rd row of the matrix[1] 3 8 13 18 23mat[2:4,1:3] # rows 2 to 4 and columns 1 to 3 [,1] [,2] [,3]

[1,] 2 7 12

[2,] 3 8 13

[3,] 4 9 14set.seed(123) # set seed for reproducibility

x <- sample(1:20, 9) # 9 random numbers

mat <- matrix(x, nrow = 3, ncol = 3) # 3x3 matrix

print(mat) # print the matrix [,1] [,2] [,3]

[1,] 15 3 6

[2,] 19 10 11

[3,] 14 2 5## Inverse Matrix

solve(mat) [,1] [,2] [,3]

[1,] -1.866667 0.2 1.8

[2,] -3.933333 0.6 3.4

[3,] 6.800000 -0.8 -6.2## Unit Matrix

mat %*% solve(mat) |> round(5) # unit matrix [,1] [,2] [,3]

[1,] 1 0 0

[2,] 0 1 0

[3,] 0 0 1Create a data frame

ID <- c(1, 2, 3, 4) # numeric vector

Color <- c("red", "white", "red", NA) # character vector

Passed <- c(TRUE, TRUE, TRUE, FALSE) # logical vector

mydata <- data.frame(ID, Color, Passed) # create data frame

# access elements of the data frame

mydata[1:2] # columns 1 and 2 of data frame ID Color

1 1 red

2 2 white

3 3 red

4 4 <NA>mydata[c("ID","Color")] # columns ID and Age from data frame ID Color

1 1 red

2 2 white

3 3 red

4 4 <NA>## Example: Data Frame

mydata <- data.frame(

ID = c(1, 2, 3, 4),

Color = c("red", "white", "red", NA),

Passed = c(TRUE, TRUE, TRUE, FALSE)

)

# mydataからColorを取り出す

mydata["Color"] Color

1 red

2 white

3 red

4 <NA># mydataからIDの3番目の要素を取り出す

mydata[3,"ID"][1] 3List

a <- b <- "seven"

z <- y <- 0

# example of a list with 4 components -

w <- list(name = "Fred", mynumbers = a, mymatrix = y, age = 5.3)

w$name

[1] "Fred"

$mynumbers

[1] "seven"

$mymatrix

[1] 0

$age

[1] 5.3list1 <- list(name = "Fred", mynumbers = a, mymatrix = y, age = 5.3)

list2 <- list(name = "Joe", mynumbers = b, mymatrix = z, age = 10.11) # 誤字

v <- c(list1,list2)

v$name

[1] "Fred"

$mynumbers

[1] "seven"

$mymatrix

[1] 0

$age

[1] 5.3

$name

[1] "Joe"

$mynumbers

[1] "seven"

$mymatrix

[1] 0

$age

[1] 10.11w[[1]] # 1st component of the list[1] "Fred"v[["mynumbers"]] # component named mynumbers in list[1] "seven"## Example: list

mylist <- list(

a <- c("one", "two", "three"),

b <- c(1,2,3),

c <- matrix(1:9, nrow = 3)

)

# mylistからaを取り出す

mylist[1][[1]]

[1] "one" "two" "three"# mylistからbの2番目の要素を取り出す

mylist[[2]][2][1] 2factor

gender <- c(rep("male", 20), rep("female", 30))

gender <- factor(gender) # ファクター型に変換

gender [1] male male male male male male male male male male

[11] male male male male male male male male male male

[21] female female female female female female female female female female

[31] female female female female female female female female female female

[41] female female female female female female female female female female

Levels: female malesummary(gender)female male

30 20 rating <- c("medium", "large", "small") # 文字ベクトル

rating <- ordered(rating, levels = c("small", "medium", "large"))

rating[1] medium large small

Levels: small < medium < largearry <- read_csv( #

system.file(

"extdata",

"morph_array.csv", #

package = "auditanalytics",

mustWork = TRUE

)

)

head(arry)# A tibble: 5 × 11

scope ben_1 cost_1 ben_2 cost_2 ben_3 cost_3 ben_4 cost_4 ben_5 cost_5

<dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 1 810 500 940 440 140 130 190 170 20 10

2 2 1370 890 1610 1010 3970 2770 3430 2460 3020 2650

3 3 9070 4850 6190 3250 5710 3590 7650 5360 7970 5220

4 4 4720 2400 4650 3950 330 260 2120 1580 2600 2020

5 5 8650 4830 9100 4060 5090 3480 8400 7540 5930 4610arry |>

kable(longtable = T) |>

kable_styling( # specify table style

bootstrap_options = c("striped", "hover", "condensed"),

full_width = F, font_size = 18

)| scope | ben_1 | cost_1 | ben_2 | cost_2 | ben_3 | cost_3 | ben_4 | cost_4 | ben_5 | cost_5 |

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 810 | 500 | 940 | 440 | 140 | 130 | 190 | 170 | 20 | 10 |

| 2 | 1370 | 890 | 1610 | 1010 | 3970 | 2770 | 3430 | 2460 | 3020 | 2650 |

| 3 | 9070 | 4850 | 6190 | 3250 | 5710 | 3590 | 7650 | 5360 | 7970 | 5220 |

| 4 | 4720 | 2400 | 4650 | 3950 | 330 | 260 | 2120 | 1580 | 2600 | 2020 |

| 5 | 8650 | 4830 | 9100 | 4060 | 5090 | 3480 | 8400 | 7540 | 5930 | 4610 |

length(arry) # 要素・コンポーネントの数[1] 11class(arry) # オブジェクトのクラス・型[1] "spec_tbl_df" "tbl_df" "tbl" "data.frame" names(arry) # オブジェクトの変数名 [1] "scope" "ben_1" "cost_1" "ben_2" "cost_2" "ben_3" "cost_3" "ben_4"

[9] "cost_4" "ben_5" "cost_5"Chapter 3. Analysis of Accounting Transactions

lubridate packages

pacman::p_load(auditanalytics, tidyverse)lubridate is a package that makes it easier to work with dates and times in R.

ymd(20101215) # year month day[1] "2010-12-15"mdy("4/1/17") # month day year[1] "2017-04-01"bday <- dmy("14/10/1979")

month(bday) # 月を取得[1] 10wday(bday, label = TRUE) # 1979年10月14日は日曜日[1] 日

Levels: 日 < 月 < 火 < 水 < 木 < 金 < 土year(bday) <- 2016

wday(bday, label = TRUE) # 2016年10月14日は金曜日[1] 金

Levels: 日 < 月 < 火 < 水 < 木 < 金 < 土Accounting Transactions for Auditors

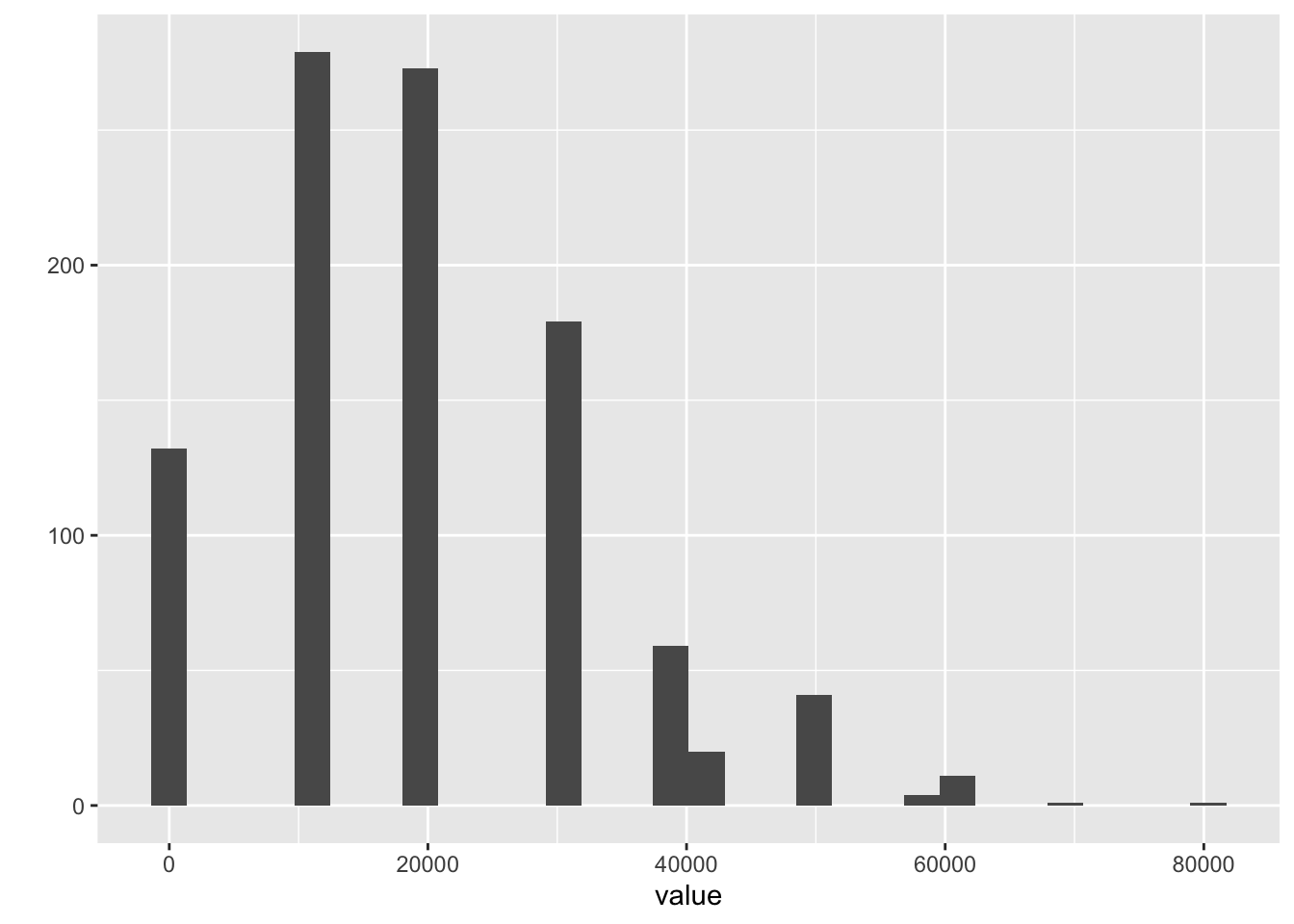

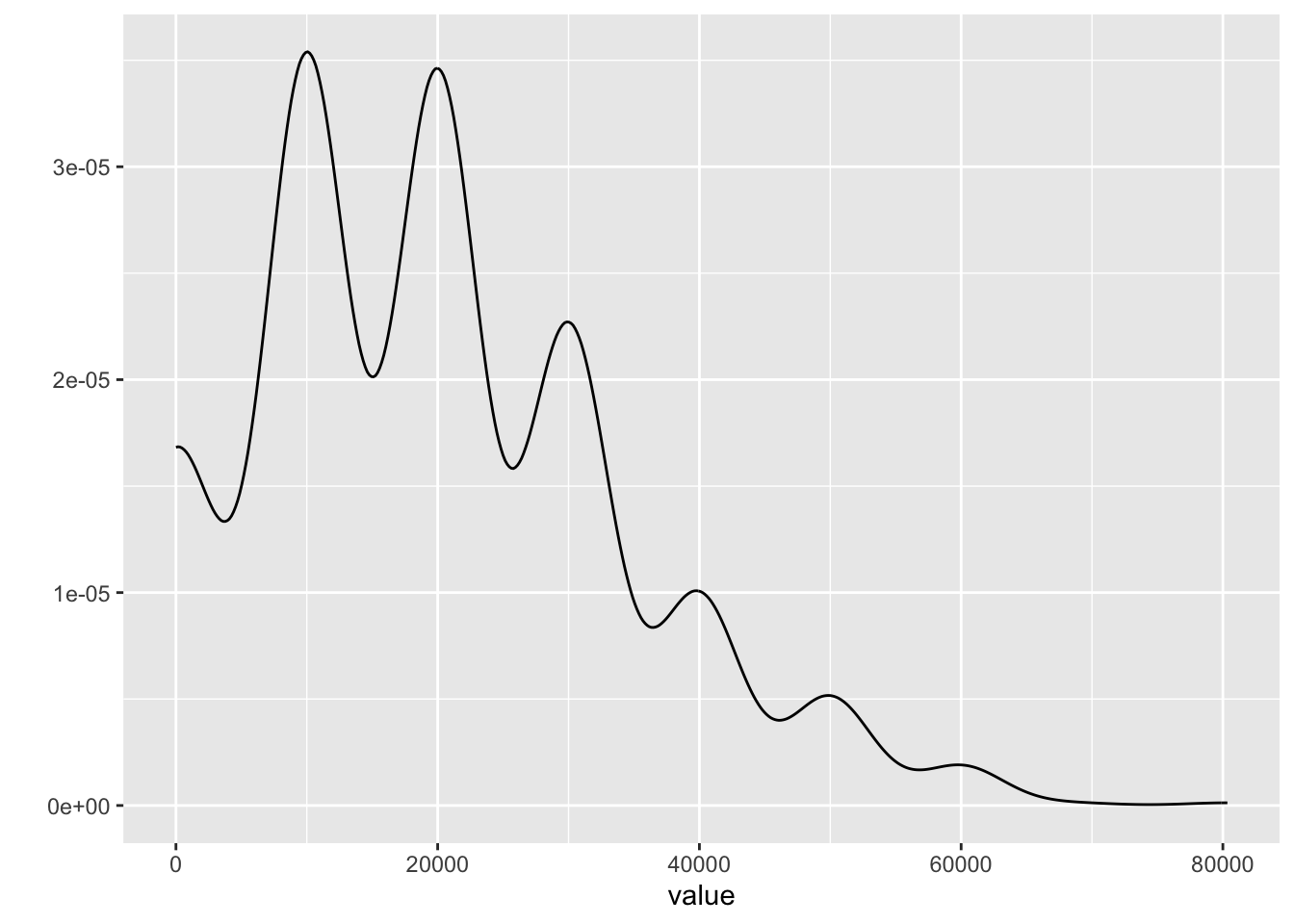

price <- rpois(n = 1000, lambda = 2) # ポワソン分布から1000個の乱数を生成

price |> head()[1] 5 2 3 2 0 4quantity <- rpois(1000, 10000) # ポワソン分布から1000個の乱数を生成

quantity |> head()[1] 9990 10001 10075 10036 9941 10021value <- price * quantity # 価格と数量の積

qplot(value, geom = "histogram") # ヒストグラム

qplot(value, geom = "density") # 密度分布

disburse <- read_csv(system.file( # csvファイルの読み込み

"extdata",

"ch_2_AP_disbursements_journal.csv", # ファイル名

package = "auditanalytics",

mustWork = TRUE

)

) # ファイルがない場合はエラーを返す

summary(disburse) # descriptive statistics disbursement_no date amount_paid

Length:50 Min. :2018-03-21 Min. :2417

Class :character 1st Qu.:2018-06-27 1st Qu.:2537

Mode :character Median :2018-10-12 Median :2618

Mean :2018-10-07 Mean :2686

3rd Qu.:2018-12-24 3rd Qu.:2800

Max. :2019-06-20 Max. :3190 # output the total amount paid

cat('\n\n 支払帳の合計金額 = ', sum(disburse$amount_paid))

支払帳の合計金額 = 134313.5library(Hmisc) # 記述統計量の計算

bank_fin <- read.csv(system.file(

"extdata",

"ch_2_yahoo_fin.csv",

package = "auditanalytics",

mustWork = TRUE

)

)

Hmisc::describe(bank_fin) # Show summary statisticsbank_fin

9 Variables 38 Observations

--------------------------------------------------------------------------------

ticker

n missing distinct

25 13 25

lowest : BAC-PC BAC-PE BAC-PK BAC-PL BAC-PY, highest: WFC-PR WFC-PV WFC-PW WFC-PX WFC-PY

--------------------------------------------------------------------------------

name

n missing distinct

25 13 7

lowest : Banco Santander, S.A. GTD PFD SECS 6 Bank of America Corporation Berkshire Hathaway Inc. HSBC Holdings plc ADR A 1/40PF A JPMorgan Chase & Co.

highest: Berkshire Hathaway Inc. HSBC Holdings plc ADR A 1/40PF A JPMorgan Chase & Co. Visa Inc. Wells Fargo & Company

--------------------------------------------------------------------------------

price

n missing distinct Info Mean Gmd .05 .10

25 13 25 1 12231 24374 22.38 22.93

.25 .50 .75 .90 .95

25.70 26.45 28.66 935.15 1437.69

Value 0e+00 3e+05

Frequency 24 1

Proportion 0.96 0.04

For the frequency table, variable is rounded to the nearest 5000

--------------------------------------------------------------------------------

change

n missing distinct

26 12 22

lowest : -0.01 -0.03 -0.04 -0.06 -0.07

highest: 0.14 1.10 1.92 2631.00 ticker

--------------------------------------------------------------------------------

percent_change

n missing distinct Info Mean Gmd .05 .10

25 13 23 0.999 0.2016 0.4513 -0.268 -0.252

.25 .50 .75 .90 .95

-0.110 0.180 0.410 0.740 0.952

lowest : -0.48 -0.27 -0.26 -0.24 -0.19, highest: 0.44 0.53 0.88 0.97 1.02

--------------------------------------------------------------------------------

volume

n missing distinct Info Mean Gmd .05 .10

25 13 25 1 520349 939507 4340 5020

.25 .50 .75 .90 .95

20982 34142 80933 1267169 3278800

lowest : 243 4284 4566 5700 11997

highest: 89764 140922 2018000 3594000 6506000

--------------------------------------------------------------------------------

vol_ave

n missing distinct Info Mean Gmd .05 .10

25 13 25 1 935629 1706024 6093 7569

.25 .50 .75 .90 .95

29831 44849 85711 2347830 6281000

Value 0 100000 3700000 6900000 11400000

Frequency 19 3 1 1 1

Proportion 0.76 0.12 0.04 0.04 0.04

For the frequency table, variable is rounded to the nearest 100000

--------------------------------------------------------------------------------

capitalization

n missing distinct

25 13 25

lowest : 211.288B 212.921B 214.807B 215.543B 216.366B

highest: 368.674B 403.496B 492.962B 493.498B 541.154B

--------------------------------------------------------------------------------

pe_ratio

n missing distinct Info Mean Gmd .05 .10

25 13 25 1 43.2 71.1 2.846 3.834

.25 .50 .75 .90 .95

5.440 7.430 11.120 53.596 249.240

Value 0 5 10 15 30 45 55 295 505

Frequency 3 15 1 1 1 1 1 1 1

Proportion 0.12 0.60 0.04 0.04 0.04 0.04 0.04 0.04 0.04

For the frequency table, variable is rounded to the nearest 5

--------------------------------------------------------------------------------library(psych) # 心理統計学のためのパッケージ

psych::describe(bank_fin) # 記述統計量の出力 vars n mean sd median trimmed mad min

ticker* 1 38 9.55 8.61 7.50 8.91 9.64 1.00

name* 2 38 4.05 2.89 3.00 3.97 2.97 1.00

price 3 25 12231.23 60356.40 26.45 112.41 1.93 20.88

change* 4 38 8.84 7.52 7.50 8.34 9.64 1.00

percent_change 5 25 0.20 0.39 0.18 0.18 0.37 -0.48

volume 6 25 520348.92 1480580.79 34142.00 138295.05 32832.18 243.00

vol_ave 7 25 935628.64 2678595.35 44849.00 237653.14 45797.51 245.00

capitalization* 8 38 9.55 8.61 7.50 8.91 9.64 1.00

pe_ratio 9 25 43.20 113.07 7.43 12.99 3.16 0.01

max range skew kurtosis se

ticker* 26.00 25.00 0.47 -1.30 1.40

name* 8.00 7.00 0.30 -1.61 0.47

price 301936.00 301915.12 4.42 18.23 12071.28

change* 23.00 22.00 0.37 -1.40 1.22

percent_change 1.02 1.50 0.41 -0.63 0.08

volume 6506000.00 6505757.00 3.01 8.48 296116.16

vol_ave 11488000.00 11487755.00 2.90 7.68 535719.07

capitalization* 26.00 25.00 0.47 -1.30 1.40

pe_ratio 506.93 506.92 3.19 9.35 22.61psych::describeBy(bank_fin, bank_fin$name)

Descriptive statistics by group

group:

vars n mean sd median trimmed mad min max range skew kurtosis

ticker 1 13 1.00 0.0 1 1 0 1 1 0 NaN NaN

name 2 13 1.00 0.0 1 1 0 1 1 0 NaN NaN

price 3 0 NaN NA NA NaN NA Inf -Inf -Inf NA NA

change 4 13 2.69 6.1 1 1 0 1 23 22 2.82 6.44

percent_change 5 0 NaN NA NA NaN NA Inf -Inf -Inf NA NA

volume 6 0 NaN NA NA NaN NA Inf -Inf -Inf NA NA

vol_ave 7 0 NaN NA NA NaN NA Inf -Inf -Inf NA NA

capitalization 8 13 1.00 0.0 1 1 0 1 1 0 NaN NaN

pe_ratio 9 0 NaN NA NA NaN NA Inf -Inf -Inf NA NA

se

ticker 0.00

name 0.00

price NA

change 1.69

percent_change NA

volume NA

vol_ave NA

capitalization 0.00

pe_ratio NA

------------------------------------------------------------

group: Banco Santander, S.A. GTD PFD SECS 6

vars n mean sd median trimmed mad min max range

ticker 1 1 15.00 NA 15.00 15.00 0 15.00 15.00 0

name 2 1 2.00 NA 2.00 2.00 0 2.00 2.00 0

price 3 1 22.72 NA 22.72 22.72 0 22.72 22.72 0

change 4 1 12.00 NA 12.00 12.00 0 12.00 12.00 0

percent_change 5 1 0.18 NA 0.18 0.18 0 0.18 0.18 0

volume 6 1 11997.00 NA 11997.00 11997.00 0 11997.00 11997.00 0

vol_ave 7 1 19388.00 NA 19388.00 19388.00 0 19388.00 19388.00 0

capitalization 8 1 20.00 NA 20.00 20.00 0 20.00 20.00 0

pe_ratio 9 1 49.93 NA 49.93 49.93 0 49.93 49.93 0

skew kurtosis se

ticker NA NA NA

name NA NA NA

price NA NA NA

change NA NA NA

percent_change NA NA NA

volume NA NA NA

vol_ave NA NA NA

capitalization NA NA NA

pe_ratio NA NA NA

------------------------------------------------------------

group: Bank of America Corporation

vars n mean sd median trimmed mad min

ticker 1 7 5.00 2.16 5.00 5.00 2.97 2.00

name 2 7 3.00 0.00 3.00 3.00 0.00 3.00

price 3 7 224.31 529.23 25.78 224.31 3.77 20.88

change 4 7 6.43 4.31 5.00 6.43 2.97 3.00

percent_change 5 7 -0.11 0.24 -0.19 -0.11 0.12 -0.27

volume 6 7 33409.00 29580.81 32345.00 33409.00 32341.44 4566.00

vol_ave 7 7 41777.29 34055.28 29831.00 41777.29 35695.08 5755.00

capitalization 8 7 15.00 2.16 15.00 15.00 2.97 12.00

pe_ratio 9 7 79.83 188.34 9.17 79.83 1.33 7.43

max range skew kurtosis se

ticker 8.00 6.00 0.00 -1.71 0.82

name 3.00 0.00 NaN NaN 0.00

price 1424.47 1403.59 1.62 0.80 200.03

change 15.00 12.00 0.98 -0.63 1.63

percent_change 0.41 0.68 1.37 0.28 0.09

volume 86124.00 81558.00 0.56 -1.25 11180.50

vol_ave 85711.00 79956.00 0.18 -2.02 12871.69

capitalization 18.00 6.00 0.00 -1.71 0.82

pe_ratio 506.93 499.50 1.62 0.80 71.18

------------------------------------------------------------

group: Berkshire Hathaway Inc.

vars n mean sd median trimmed mad

ticker 1 2 9.50 0.71 9.50 9.50 0.74

name 2 2 4.00 0.00 4.00 4.00 0.00

price 3 2 151068.58 213358.75 151068.58 151068.58 223676.04

change 4 2 21.50 0.71 21.50 21.50 0.74

percent_change 5 2 0.92 0.06 0.92 0.92 0.07

volume 6 2 1009121.50 1426769.66 1009121.50 1009121.50 1495763.26

vol_ave 7 2 1890622.50 2673397.50 1890622.50 1890622.50 2802673.68

capitalization 8 2 24.50 0.71 24.50 24.50 0.74

pe_ratio 9 2 8.57 12.11 8.57 8.57 12.70

min max range skew kurtosis se

ticker 9.00 10.00 1.00 0 -2.75 0.50

name 4.00 4.00 0.00 NaN NaN 0.00

price 201.16 301936.00 301734.84 0 -2.75 150867.42

change 21.00 22.00 1.00 0 -2.75 0.50

percent_change 0.88 0.97 0.09 0 -2.75 0.04

volume 243.00 2018000.00 2017757.00 0 -2.75 1008878.50

vol_ave 245.00 3781000.00 3780755.00 0 -2.75 1890377.50

capitalization 24.00 25.00 1.00 0 -2.75 0.50

pe_ratio 0.01 17.14 17.13 0 -2.75 8.56

------------------------------------------------------------

group: HSBC Holdings plc ADR A 1/40PF A

vars n mean sd median trimmed mad min max range

ticker 1 1 11.00 NA 11.00 11.00 0 11.00 11.00 0

name 2 1 5.00 NA 5.00 5.00 0 5.00 5.00 0

price 3 1 26.45 NA 26.45 26.45 0 26.45 26.45 0

change 4 1 10.00 NA 10.00 10.00 0 10.00 10.00 0

percent_change 5 1 0.00 NA 0.00 0.00 0 0.00 0.00 0

volume 6 1 26376.00 NA 26376.00 26376.00 0 26376.00 26376.00 0

vol_ave 7 1 61496.00 NA 61496.00 61496.00 0 61496.00 61496.00 0

capitalization 8 1 26.00 NA 26.00 26.00 0 26.00 26.00 0

pe_ratio 9 1 56.04 NA 56.04 56.04 0 56.04 56.04 0

skew kurtosis se

ticker NA NA NA

name NA NA NA

price NA NA NA

change NA NA NA

percent_change NA NA NA

volume NA NA NA

vol_ave NA NA NA

capitalization NA NA NA

pe_ratio NA NA NA

------------------------------------------------------------

group: JPMorgan Chase & Co.

vars n mean sd median trimmed mad

ticker 1 3 13.00 1.00 13.00 13.00 1.48

name 2 3 6.00 0.00 6.00 6.00 0.00

price 3 3 54.84 46.66 28.05 54.84 0.44

change 4 3 12.67 9.45 16.00 12.67 5.93

percent_change 5 3 0.45 0.54 0.36 0.45 0.59

volume 6 3 2225376.33 3707131.82 89764.00 2225376.33 13934.96

vol_ave 7 3 3941765.67 6535296.89 198076.00 3941765.67 87258.42

capitalization 8 3 20.67 1.53 21.00 20.67 1.48

pe_ratio 9 3 5.61 4.77 2.87 5.61 0.04

min max range skew kurtosis se

ticker 12.00 1.4000e+01 2.00 0.00 -2.33 0.58

name 6.00 6.0000e+00 0.00 NaN NaN 0.00

price 27.75 1.0871e+02 80.96 0.38 -2.33 26.94

change 2.00 2.0000e+01 18.00 -0.31 -2.33 5.46

percent_change -0.04 1.0200e+00 1.06 0.16 -2.33 0.31

volume 80365.00 6.5060e+06 6425635.00 0.38 -2.33 2140313.55

vol_ave 139221.00 1.1488e+07 11348779.00 0.38 -2.33 3773155.42

capitalization 19.00 2.2000e+01 3.00 -0.21 -2.33 0.88

pe_ratio 2.84 1.1120e+01 8.28 0.38 -2.33 2.76

------------------------------------------------------------

group: Visa Inc.

vars n mean sd median trimmed mad min

ticker 1 1 16.00 NA 16.00 16.00 0 16.00

name 2 1 7.00 NA 7.00 7.00 0 7.00

price 3 1 180.07 NA 180.07 180.07 0 180.07

change 4 1 7.00 NA 7.00 7.00 0 7.00

percent_change 5 1 -0.48 NA -0.48 -0.48 0 -0.48

volume 6 1 3594000.00 NA 3594000.00 3594000.00 0 3594000.00

vol_ave 7 1 6906000.00 NA 6906000.00 6906000.00 0 6906000.00

capitalization 8 1 23.00 NA 23.00 23.00 0 23.00

pe_ratio 9 1 34.58 NA 34.58 34.58 0 34.58

max range skew kurtosis se

ticker 16.00 0 NA NA NA

name 7.00 0 NA NA NA

price 180.07 0 NA NA NA

change 7.00 0 NA NA NA

percent_change -0.48 0 NA NA NA

volume 3594000.00 0 NA NA NA

vol_ave 6906000.00 0 NA NA NA

capitalization 23.00 0 NA NA NA

pe_ratio 34.58 0 NA NA NA

------------------------------------------------------------

group: Wells Fargo & Company

vars n mean sd median trimmed mad min

ticker 1 10 21.50 3.03 21.50 21.50 3.71 17.00

name 2 10 8.00 0.00 8.00 8.00 0.00 8.00

price 3 10 167.96 447.30 26.42 26.63 0.90 25.58

change 4 10 14.60 3.57 15.50 14.88 3.71 8.00

percent_change 5 10 0.29 0.19 0.36 0.31 0.15 -0.07

volume 6 10 44811.50 39786.63 32546.00 37863.62 16703.71 4284.00

vol_ave 7 10 50484.90 35897.76 39847.00 44781.88 14567.29 7758.00

capitalization 8 10 6.50 3.03 6.50 6.50 3.71 2.00

pe_ratio 9 10 34.68 92.36 5.46 5.50 0.19 5.28

max range skew kurtosis se

ticker 26.00 9.00 0.00 -1.56 0.96

name 8.00 0.00 NaN NaN 0.00

price 1441.00 1415.42 2.28 3.57 141.45

change 19.00 11.00 -0.42 -1.31 1.13

percent_change 0.53 0.60 -0.56 -1.13 0.06

volume 140922.00 136638.00 1.31 0.62 12581.64

vol_ave 138836.00 131078.00 1.31 0.92 11351.87

capitalization 11.00 9.00 0.00 -1.56 0.96

pe_ratio 297.54 292.26 2.28 3.57 29.21pacman::p_load(kableExtra, broom, pastecs) # パッケージの読み込み

## Tidy these up and write them as a formated table, using kableExtra

pastecs::stat.desc(bank_fin) |> # 記述統計量の計算

broom::tidy() |> # データフレームに変換

kable(longtable = T, caption = "Summary Statistics") |>

kable_styling(full_width = F, font_size = 18)| column | n | mean | sd | median | trimmed | mad | min | max | range | skew | kurtosis | se |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ticker | 0 | NaN | NA | NA | NaN | NA | Inf | -Inf | -Inf | NA | NA | NA |

| name | 0 | NaN | NA | NA | NaN | NA | Inf | -Inf | -Inf | NA | NA | NA |

| price | 14 | 2.602796e+08 | 9.735837e+08 | 1.215125e+04 | 8.494124e+04 | 1.214879e+04 | 0.00 | 3.642895e+09 | 3.642895e+09 | 3.328201 | 12.076923 | 2.602012e+08 |

| change | 0 | NaN | NA | NA | NaN | NA | Inf | -Inf | -Inf | NA | NA | NA |

| percent_change | 14 | 3.515023e+00 | 7.098547e+00 | 6.972503e-01 | 2.057527e+00 | 5.799849e-01 | -0.48 | 2.500000e+01 | 2.548000e+01 | 2.331536 | 7.251627 | 1.897167e+00 |

| volume | 14 | 1.565820e+11 | 5.858680e+11 | 4.082325e+05 | 2.413592e+06 | 4.082246e+05 | 0.00 | 2.192119e+12 | 2.192119e+12 | 3.328201 | 12.076923 | 1.565798e+11 |

| vol_ave | 14 | 5.124946e+11 | 1.917564e+12 | 7.356739e+05 | 4.305602e+06 | 7.356659e+05 | 0.00 | 7.174873e+12 | 7.174873e+12 | 3.328201 | 12.076923 | 5.124906e+11 |

| capitalization | 0 | NaN | NA | NA | NaN | NA | Inf | -Inf | -Inf | NA | NA | NA |

| pe_ratio | 14 | 1.082288e+03 | 3.382558e+03 | 3.410240e+01 | 1.972988e+02 | 3.278888e+01 | 0.00 | 1.278445e+04 | 1.278445e+04 | 3.280235 | 11.874574 | 9.040266e+02 |

QQ-Plot

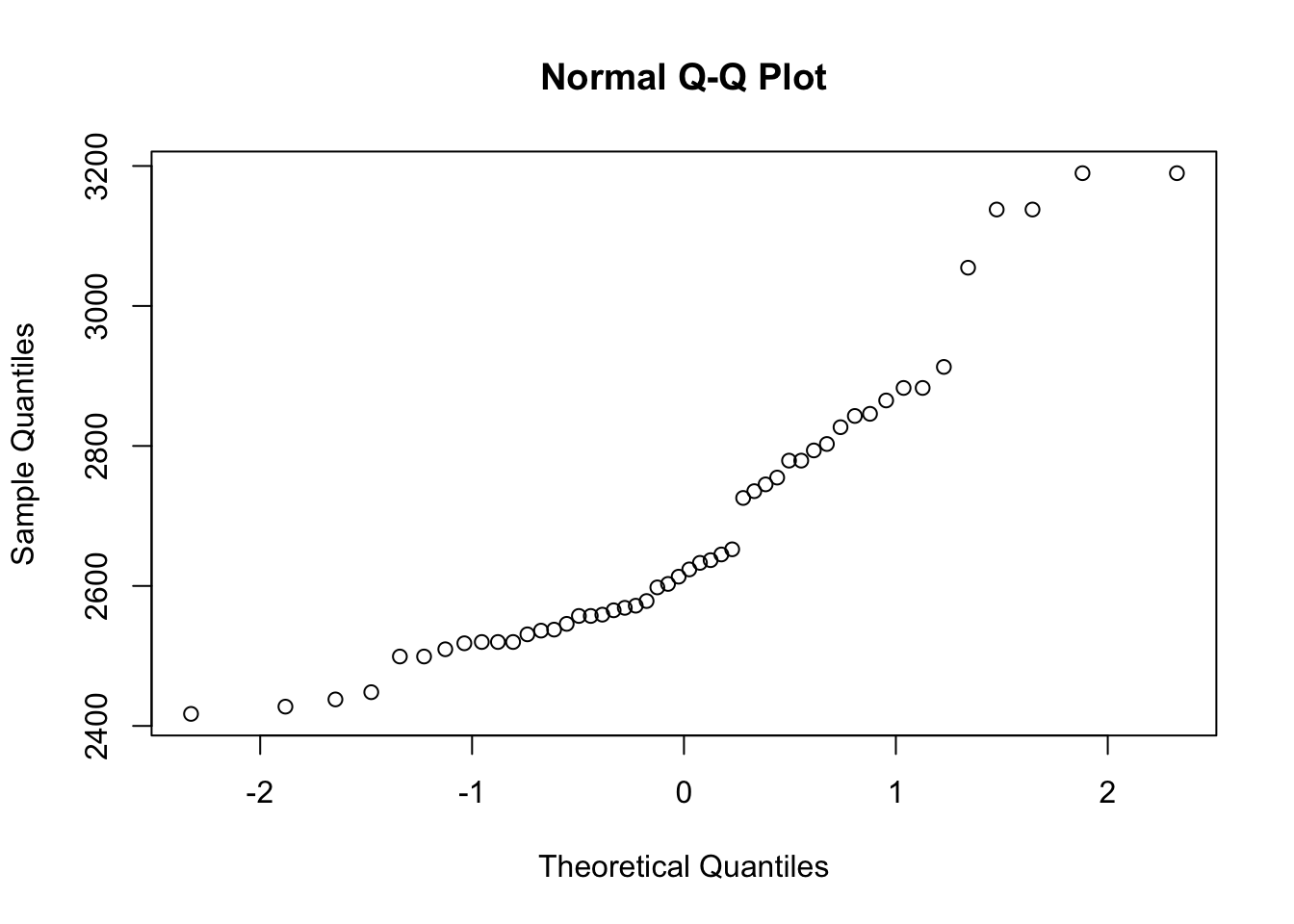

disburse <- readr::read_csv(system.file(

"extdata",

"ch_2_AP_disbursements_journal.csv", # csv file

package = "auditanalytics",

mustWork = TRUE

)

)

head(disburse)# A tibble: 6 × 3

disbursement_no date amount_paid

<chr> <date> <dbl>

1 dis00001 2018-03-21 2883.

2 dis00002 2018-04-11 2598.

3 dis00003 2018-04-18 3138.

4 dis00004 2018-04-22 2518.

5 dis00005 2018-04-26 2520.

6 dis00006 2018-05-16 2843.d <- as.numeric(as.character(disburse$amount_paid))

head(d)[1] 2882.88 2597.91 3137.78 2518.08 2519.91 2842.84class(d)[1] "numeric"qqnorm(d,

main = "Normal Q-Q Plot", # QQプロットを作成

xlab = "Theoretical Quantiles", # x軸のラベル

ylab = "Sample Quantiles", # y軸のラベル

plot.it = TRUE) # プロットするかどうか

Density and Cumulative Distribution

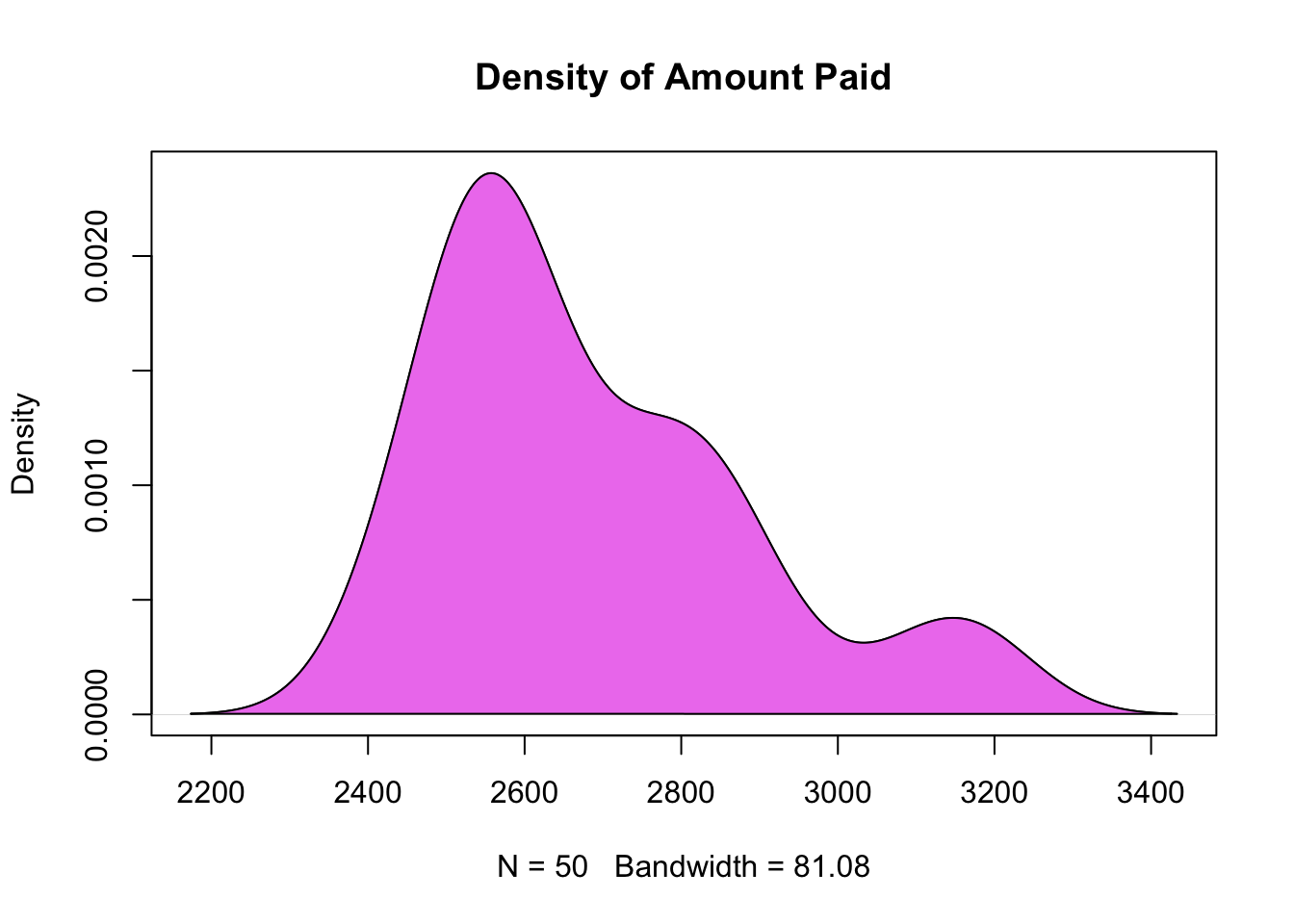

d <- density(disburse$amount_paid) # density of amount paid

plot(d, main = "Density of Amount Paid") # plot density

polygon(d, col="violet", border="black") # add color

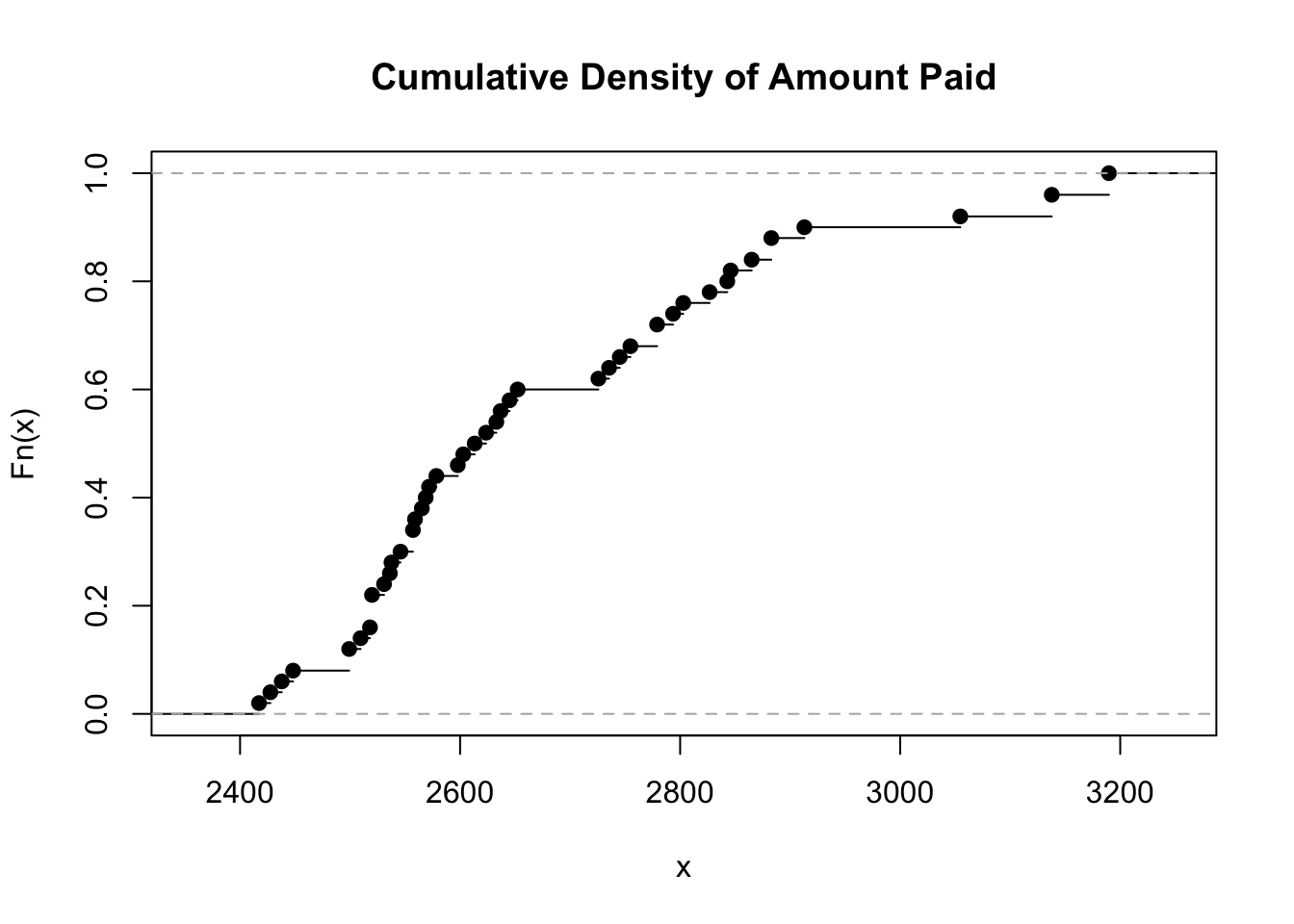

plot(

ecdf(disburse$amount_paid), # 累積分布関数を計算

main = "Cumulative Density of Amount Paid" # 図のタイトル

) # 誤植 ~いらない

ecdf() is a function that computes the empirical cumulative distribution function of a dataset.

lr <- read_csv(system.file(

"extdata",

"ch_2_data_types.csv",

package = "auditanalytics",

mustWork = TRUE

)

)

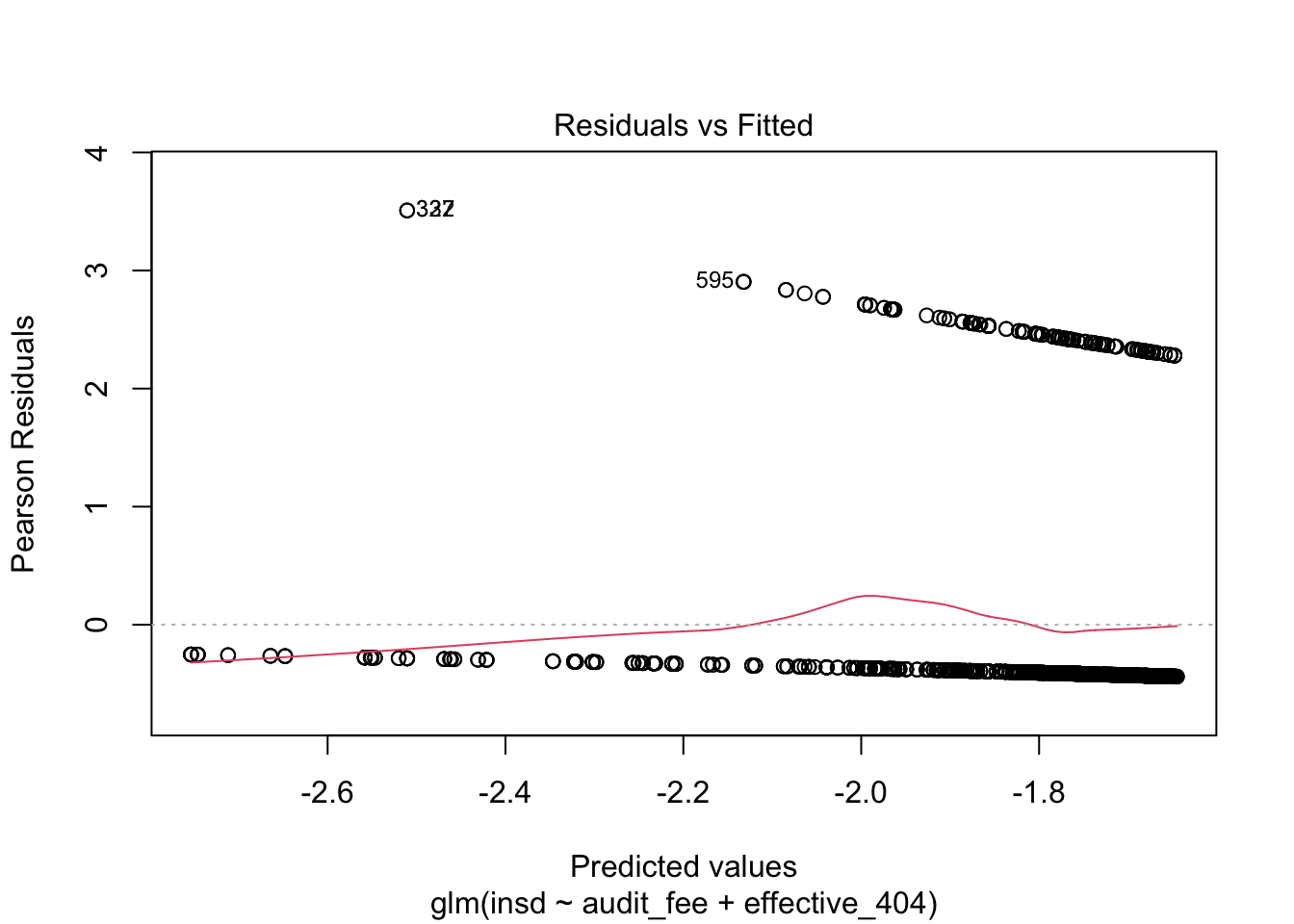

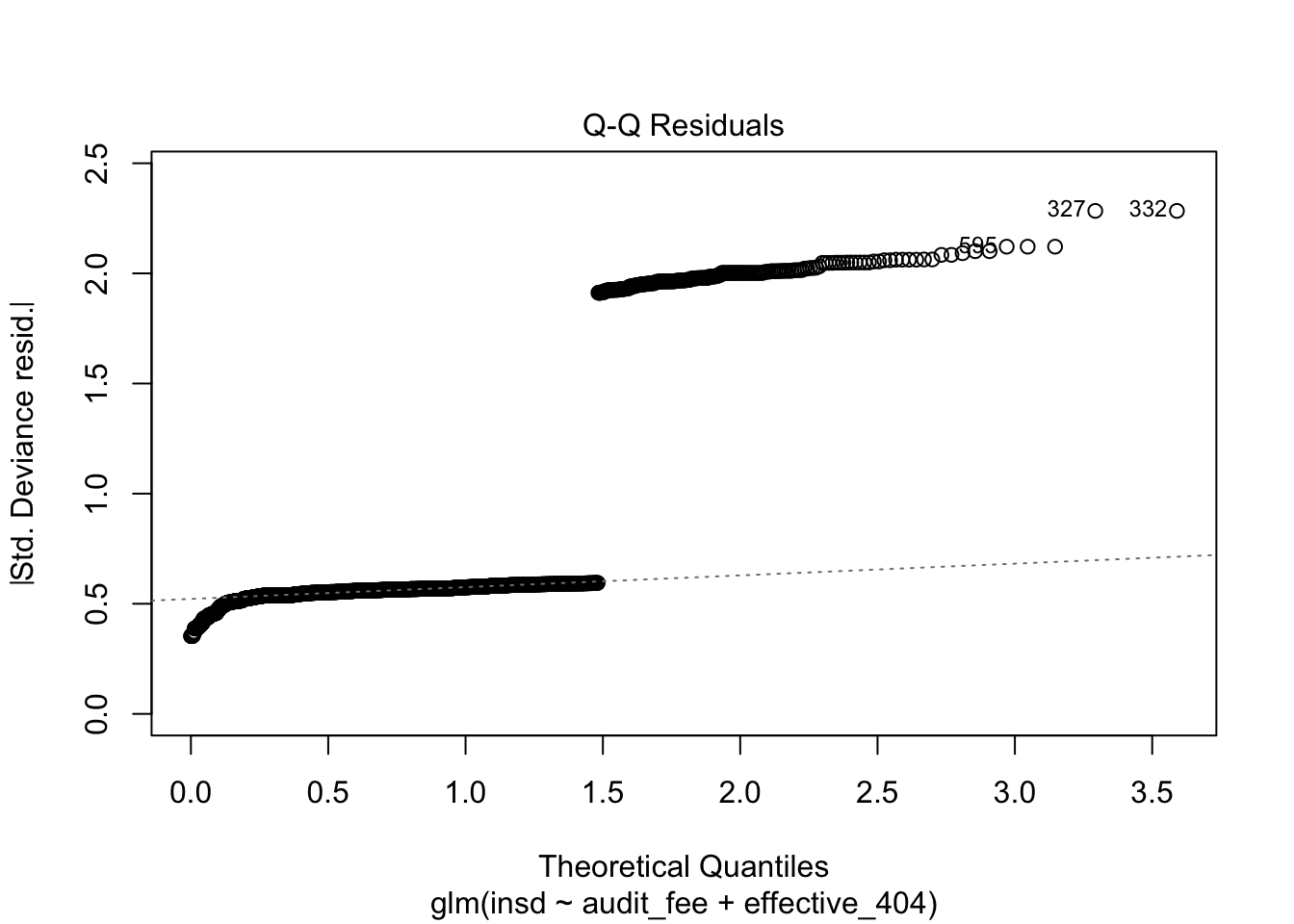

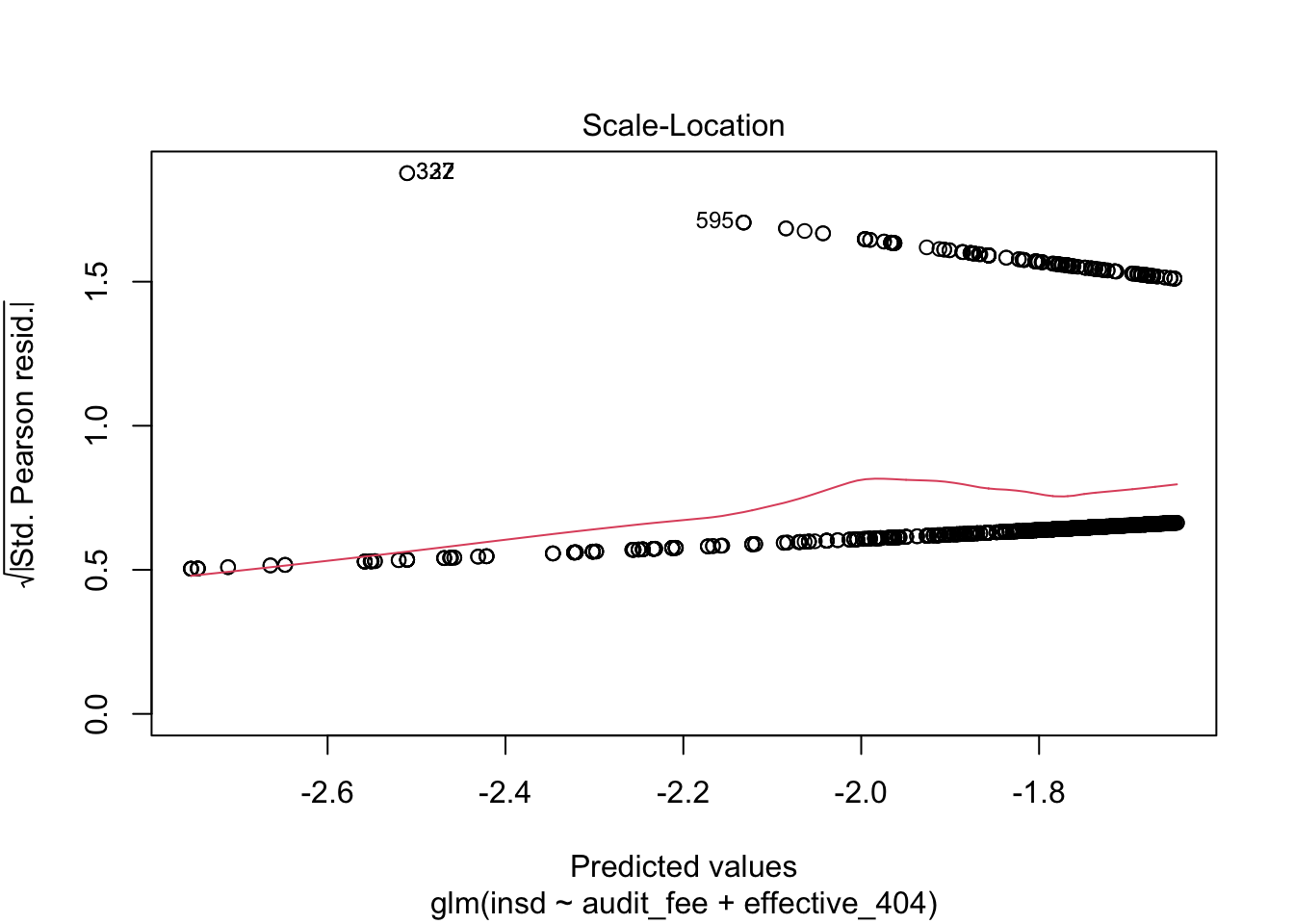

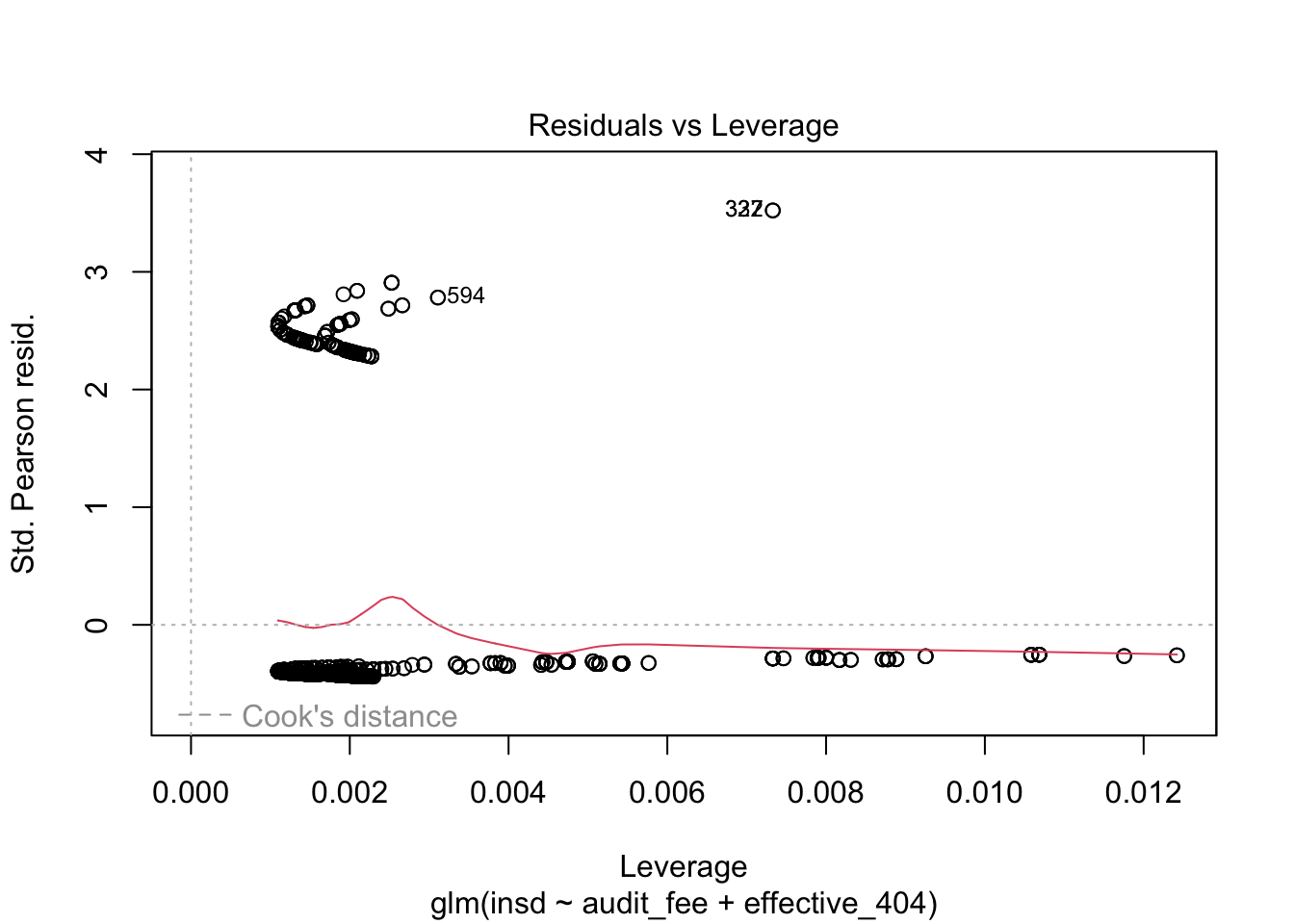

lgt <- glm( # general linear method

formula = insd ~ audit_fee + effective_404, # 回帰モデル

family = "binomial", # link function

data = lr) # data frame

summary(lgt) # 結果の表示

Call:

glm(formula = insd ~ audit_fee + effective_404, family = "binomial",

data = lr)

Coefficients:

Estimate Std. Error z value Pr(>|z|)

(Intercept) -1.732e+00 1.128e-01 -15.354 <2e-16 ***

audit_fee -9.530e-09 4.496e-09 -2.120 0.034 *

effective_404 8.928e-02 1.518e-01 0.588 0.557

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

(Dispersion parameter for binomial family taken to be 1)

Null deviance: 1214.8 on 1511 degrees of freedom

Residual deviance: 1209.4 on 1509 degrees of freedom

(2 個の観測値が欠損のため削除されました)

AIC: 1215.4

Number of Fisher Scoring iterations: 4plot(lgt) # 図の作成

keras

# install.packages("keras") # install keras packages

library(keras)

# install_keras() # Run this only once. Installation takes time.

mnist <- dataset_mnist() # MNISTデータを読み込む

class(mnist) # List class[1] "list"glimpse(mnist) # See the structure of the dataList of 2

$ train:List of 2

..$ x: int [1:60000, 1:28, 1:28] 0 0 0 0 0 0 0 0 0 0 ...

..$ y: int [1:60000(1d)] 5 0 4 1 9 2 1 3 1 4 ...

$ test :List of 2

..$ x: int [1:10000, 1:28, 1:28] 0 0 0 0 0 0 0 0 0 0 ...

..$ y: int [1:10000(1d)] 7 2 1 0 4 1 4 9 5 9 ...The MNIST database was constructed from NIST’s Special Database 3 and Special Database 1 which contain binary images of handwritten digits.

train_images <- mnist$train$x # image data for training

train_labels <- mnist$train$y # label data for training

test_images <- mnist$test$x # test image data

test_labels <- mnist$test$y # test label data

network <- keras_model_sequential() # null model

network |>

# 28*28 pixel images are flattened into 784 pixel vectors

layer_dense(units = 512, input_shape = c(28 * 28)) |>

# ReLU activation function converts negative values to zero

layer_activation('relu') |> # ReLU activation function

layer_dense(units = 10) |> # 10 output layers 1:10

# softmax activation function convert the output to a probability distribution

layer_activation("softmax") # softmax activation function

network |> compile( # モデルをコンパイル

optimizer = "rmsprop", # 最適化アルゴリズム

loss = "categorical_crossentropy", # 損失関数

metrics = c("accuracy") # 評価関数

)

# Training data

train_images <- array_reshape( # 行列に変換

train_images, # 訓練用画像データ

c(60000, 28 * 28) # 画像の形状

)

# Test data

test_images <- array_reshape( # 行列に変換

test_images, # テスト用画像データ

c(10000, 28 * 28) # 画像の形状

)

# 0が黒,255が白のデータを0-1の範囲に正規化

train_images <- train_images / 255

test_images <- test_images / 255

train_labels <- to_categorical(train_labels) #

test_labels <- to_categorical(test_labels) #

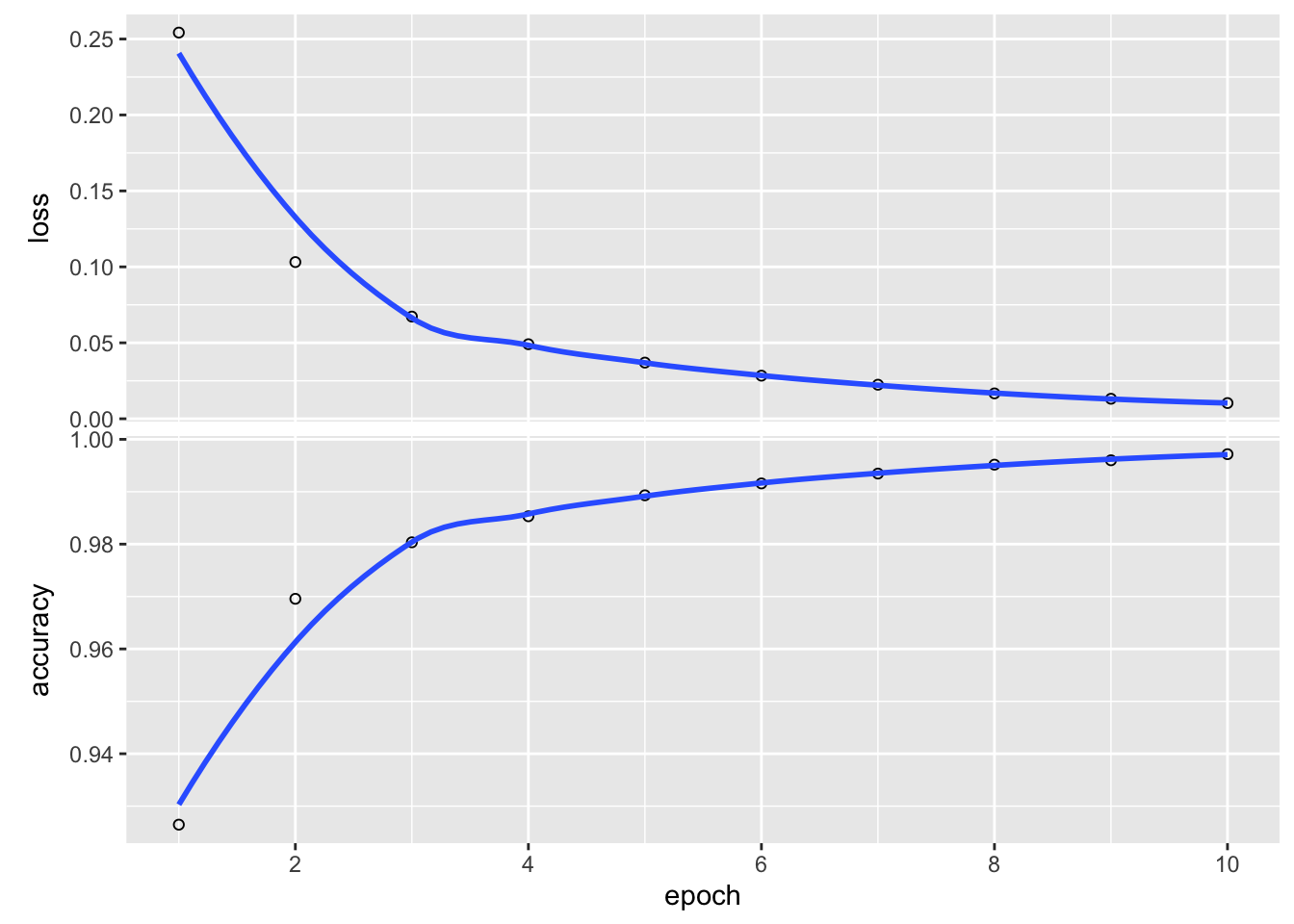

history <- network |>

fit( # training the model

train_images, # training image data

train_labels, # training label data

epochs = 10, # the number of times the model will be trained

batch_size = 128 # the number of samples per gradient update

)Epoch 1/10

469/469 - 1s - loss: 0.2542 - accuracy: 0.9265 - 1s/epoch - 3ms/step

Epoch 2/10

469/469 - 1s - loss: 0.1031 - accuracy: 0.9696 - 1s/epoch - 3ms/step

Epoch 3/10

469/469 - 1s - loss: 0.0673 - accuracy: 0.9804 - 1s/epoch - 3ms/step

Epoch 4/10

469/469 - 1s - loss: 0.0491 - accuracy: 0.9853 - 1s/epoch - 3ms/step

Epoch 5/10

469/469 - 1s - loss: 0.0370 - accuracy: 0.9893 - 1s/epoch - 3ms/step

Epoch 6/10

469/469 - 1s - loss: 0.0284 - accuracy: 0.9916 - 1s/epoch - 3ms/step

Epoch 7/10

469/469 - 1s - loss: 0.0224 - accuracy: 0.9935 - 1s/epoch - 3ms/step

Epoch 8/10

469/469 - 1s - loss: 0.0167 - accuracy: 0.9952 - 1s/epoch - 3ms/step

Epoch 9/10

469/469 - 1s - loss: 0.0132 - accuracy: 0.9960 - 1s/epoch - 3ms/step

Epoch 10/10

469/469 - 1s - loss: 0.0103 - accuracy: 0.9972 - 1s/epoch - 3ms/stepplot(history) # 訓練の履歴をプロット

metrics <- network |>

evaluate(test_images, test_labels, verbose = 0)

metrics |> kable()| x | |

|---|---|

| loss | 0.0665813 |

| accuracy | 0.9820000 |

Chapter 4. Risk Assessment and Audit Planning

Auditing

pacman::p_load(finstr, XBRL, xbrlus, pander, knitr, kableExtra)

old_o <- options(stringsAsFactors = FALSE) # 文字列をファクターとして扱わない

xbrl_data_2016 <- xbrlDoAll("XBRL/gm-20161231.xml")

xbrl_data_2017 <- xbrlDoAll("XBRL/gm-20171231.xml")

options(old_o) # 文字列をファクターとして扱う

st2016 <- xbrl_get_statements(xbrl_data_2016)

st2017 <- xbrl_get_statements(xbrl_data_2017)

print(st2017) # 2017年度の財務諸表Financial statements repository

From To Rows Columns

ConsolidatedBalanceSheets 2016-12-31 2017-12-31 2 44

ConsolidatedIncomeStatements 2015-12-31 2017-12-31 3 29

ConsolidatedStatementsOfCashFlows 2015-12-31 2017-12-31 3 42

ConsolidatedStatementsOfComprehensiveIncome 2015-12-31 2017-12-31 3 11# 連結貸借対照表を取得

balance_sheet2017 <- st2017$ConsolidatedBalanceSheets

balance_sheet2016 <- st2016$ConsolidatedBalanceSheets

# 連結損益計算書

income2017 <- st2017$ConsolidatedIncomeStatements

income2016 <- st2016$ConsolidatedIncomeStatements

## 貸借対照表を出力

capture.output(

bs_table <- print( # 出力

balance_sheet2017, # オブジェクト名

html = FALSE, # html出力しない

big.mark = ",", # 3桁区切りにカンマを使用

dateFormat = "%Y"), # 日付のフォーマット

file= "NUL") # 出力先をNULにする

bs_table |>

head(10) |> # 先頭10行を表示

kable(

longtable = T, # ページまたぎ

caption = "Balance Sheet", # タイトル

booktabs = T

) |>

kable_styling(

bootstrap_options = c("striped", "hover", "condensed"),

full_width = F,

font_siz = 18

)| Element | 2017-12-31 | 2016-12-31 |

|---|---|---|

| Assets = | 212482 | 221690 |

| + AssetsCurrent = | 68744 | 76203 |

| + CashAndCashEquivalentsAtCarryingValue | 15512 | 12574 |

| + MarketableSecuritiesCurrent | 8313 | 11841 |

| + AccountsNotesAndLoansReceivableNetCurrent | 8164 | 8700 |

| + InventoryNet | 10663 | 11040 |

| + gm_AssetsSubjecttoorAvailableforOperatingLeaseNetCurrent | 1106 | 1110 |

| + OtherAssetsCurrent | 4465 | 3633 |

| + AssetsOfDisposalGroupIncludingDiscontinuedOperationCurrent | 0 | 11178 |

| + NotesAndLoansReceivableNetCurrent | 0 | 0 |

balance_sheet <- balance_sheet2017 |> merge(balance_sheet2016)

capture.output(

bs_table <- print(

balance_sheet,

html = FALSE,

big.mark = ",",

dateFormat = "%Y"

),

file = "NUL"

)

bs_table |>

head(10) |>

kable(

longtable = T,

caption="Merged Balance Sheet",

# "latex",

booktabs = T) |>

kable_styling(

bootstrap_options = c("striped", "hover", "condensed"),

full_width = F,

font_size = 18

)| Element | 2017-12-31 | 2016-12-31 | 2015-12-31 |

|---|---|---|---|

| Assets = | 212482 | 221690 | 194338 |

| + AssetsCurrent = | 68744 | 76203 | 69408 |

| + CashAndCashEquivalentsAtCarryingValue | 15512 | 12960 | 15238 |

| + MarketableSecuritiesCurrent | 8313 | 11841 | 8163 |

| + AccountsNotesAndLoansReceivableNetCurrent | 8164 | 9638 | 8337 |

| + InventoryNet | 10663 | 13788 | 13764 |

| + gm_AssetsSubjecttoorAvailableforOperatingLeaseNetCurrent | 1106 | 1896 | 2783 |

| + OtherAssetsCurrent | 4465 | 4015 | 3072 |

| + AssetsOfDisposalGroupIncludingDiscontinuedOperationCurrent | 0 | 0 | 0 |

| + NotesAndLoansReceivableNetCurrent | 0 | 0 | 0 |

check <- check_statement(balance_sheet2017)

checkNumber of errors: 8

Number of elements in errors: 4

Element: AssetsCurrent = + CashAndCashEquivalentsAtCarryingValue + MarketableSecuritiesCurrent + AccountsNotesAndLoansReceivableNetCurrent + InventoryNet + gm_AssetsSubjecttoorAvailableforOperatingLeaseNetCurrent + OtherAssetsCurrent + AssetsOfDisposalGroupIncludingDiscontinuedOperationCurrent + NotesAndLoansReceivableNetCurrent

date original calculated error

3 2016-12-31 7.6203e+10 6.0076e+10 1.6127e+10

4 2017-12-31 6.8744e+10 4.8223e+10 2.0521e+10

Element: AssetsNoncurrent = + EquityMethodInvestments + PropertyPlantAndEquipmentNet + IntangibleAssetsNetIncludingGoodwill + DeferredIncomeTaxAssetsNet + OtherAssetsNoncurrent + DisposalGroupIncludingDiscontinuedOperationAssetsNoncurrent + NotesAndLoansReceivableNetNoncurrent + PropertySubjectToOrAvailableForOperatingLeaseNet

date original calculated error

5 2016-12-31 1.45487e+11 1.28486e+11 1.7001e+10

6 2017-12-31 1.43738e+11 1.22530e+11 2.1208e+10

Element: LiabilitiesCurrent = + AccountsPayableCurrent + AccruedLiabilitiesCurrent + LiabilitiesOfDisposalGroupIncludingDiscontinuedOperationCurrent + DebtCurrent

date original calculated error

11 2016-12-31 8.5181e+10 6.1384e+10 2.3797e+10

12 2017-12-31 7.6890e+10 4.9925e+10 2.6965e+10

Element: LiabilitiesNoncurrent = + OtherPostretirementDefinedBenefitPlanLiabilitiesNoncurrent + DefinedBenefitPensionPlanLiabilitiesNoncurrent + OtherLiabilitiesNoncurrent + LiabilitiesOfDisposalGroupIncludingDiscontinuedOperationNoncurrent + LongTermDebtAndCapitalLeaseObligations

date original calculated error

13 2016-12-31 9.2434e+10 4.1108e+10 5.1326e+10

14 2017-12-31 9.9392e+10 3.2138e+10 6.7254e+10check_statement(

within(balance_sheet2017, InventoryNet <- InventoryNet * 2)

)Number of errors: 8

Number of elements in errors: 4

Element: AssetsCurrent = + CashAndCashEquivalentsAtCarryingValue + MarketableSecuritiesCurrent + AccountsNotesAndLoansReceivableNetCurrent + InventoryNet + gm_AssetsSubjecttoorAvailableforOperatingLeaseNetCurrent + OtherAssetsCurrent + AssetsOfDisposalGroupIncludingDiscontinuedOperationCurrent + NotesAndLoansReceivableNetCurrent

date original calculated error

3 2016-12-31 7.6203e+10 7.1116e+10 5.087e+09

4 2017-12-31 6.8744e+10 5.8886e+10 9.858e+09

Element: AssetsNoncurrent = + EquityMethodInvestments + PropertyPlantAndEquipmentNet + IntangibleAssetsNetIncludingGoodwill + DeferredIncomeTaxAssetsNet + OtherAssetsNoncurrent + DisposalGroupIncludingDiscontinuedOperationAssetsNoncurrent + NotesAndLoansReceivableNetNoncurrent + PropertySubjectToOrAvailableForOperatingLeaseNet

date original calculated error

5 2016-12-31 1.45487e+11 1.28486e+11 1.7001e+10

6 2017-12-31 1.43738e+11 1.22530e+11 2.1208e+10

Element: LiabilitiesCurrent = + AccountsPayableCurrent + AccruedLiabilitiesCurrent + LiabilitiesOfDisposalGroupIncludingDiscontinuedOperationCurrent + DebtCurrent

date original calculated error

11 2016-12-31 8.5181e+10 6.1384e+10 2.3797e+10

12 2017-12-31 7.6890e+10 4.9925e+10 2.6965e+10

Element: LiabilitiesNoncurrent = + OtherPostretirementDefinedBenefitPlanLiabilitiesNoncurrent + DefinedBenefitPensionPlanLiabilitiesNoncurrent + OtherLiabilitiesNoncurrent + LiabilitiesOfDisposalGroupIncludingDiscontinuedOperationNoncurrent + LongTermDebtAndCapitalLeaseObligations

date original calculated error

13 2016-12-31 9.2434e+10 4.1108e+10 5.1326e+10

14 2017-12-31 9.9392e+10 3.2138e+10 6.7254e+10check <- check_statement(income2017, element_id = "OperatingIncomeLoss")

checkNumber of errors: 0

Number of elements in errors: 0 check$expression[1][1] "+ Revenues - CostsAndExpenses"check$calculated / 10^6[1] 5538 9962 10016Rearranging the Statement

expose() function

expose(balance_sheet,

# Assets

"Current Assets" = "AssetsCurrent",

"Noncurrent Assets" = other("Assets"),

# Liabilites and equity

"Current Liabilities" = "LiabilitiesCurrent",

"Noncurrent Liabilities" = other(c("Liabilities", "CommitmentsAndContingencies")),

"Stockholders Equity" = "StockholdersEquity"

)Financial statement: 3 observations from 2015-12-31 to 2017-12-31

Element 2017-12-31 2016-12-31 2015-12-31

Assets = 212482 221690 194338

+ Current.Assets 48223 54138 51357

+ Noncurrent.Assets 122530 90237 86258

LiabilitiesAndStockholdersEquity = 212482 221690 194338

+ Current.Liabilities 49925 56153 51655

+ Noncurrent.Liabilities 32138 36834 39249

+ Stockholders.Equity 35001 43836 39871

+ OtherLiabilitiesAndStockholdersEquity_ 1199 239 452 expose(balance_sheet,

# Assets

"Tangible Assets" = "Assets" %without% c(

"AssetsOfDisposalGroupIncludingDiscontinuedOperationCurrent",

"NotesAndLoansReceivableNetCurrent",

"gm_AssetsSubjecttoorAvailableforOperatingLeaseNetCurrent"

),

"Intangible Assets" = other("Assets"),

# Liabilites and equity

"Liabilities" = c("Liabilities", "CommitmentsAndContingencies"),

"Stockholders Equity" = "StockholdersEquity"

)Financial statement: 3 observations from 2015-12-31 to 2017-12-31

Element 2017-12-31 2016-12-31 2015-12-31

Assets = 212482 221690 194338

+ Tangible.Assets 169647 142479 134832

+ Intangible.Assets 1106 1896 2783

LiabilitiesAndStockholdersEquity = 212482 221690 194338

+ Liabilities 82063 92987 90904

+ Stockholders.Equity 35001 43836 39871

+ OtherLiabilitiesAndStockholdersEquity_ 1199 239 452 diff_bs <- diff(balance_sheet)

capture.output(

bs_table <- print(

diff_bs,

html = FALSE,

big.mark = ",",

dateFormat = "%Y"

), file = "NUL")

bs_table |>

head(10) |>

kable(longtable = T,

caption = "Lagged Differences in Balance Sheets",

# "latex",

booktabs = T) |>

kable_styling(

bootstrap_options = c("striped", "hover", "condensed"),

full_width = F,

font_size = 18)| Element | 2017-12-31 | 2016-12-31 |

|---|---|---|

| Assets = | -9208 | 27352 |

| + AssetsCurrent = | -7459 | 6795 |

| + CashAndCashEquivalentsAtCarryingValue | 2552 | -2278 |

| + MarketableSecuritiesCurrent | -3528 | 3678 |

| + AccountsNotesAndLoansReceivableNetCurrent | -1474 | 1301 |

| + InventoryNet | -3125 | 24 |

| + gm_AssetsSubjecttoorAvailableforOperatingLeaseNetCurrent | -790 | -887 |

| + OtherAssetsCurrent | 450 | 943 |

| + AssetsOfDisposalGroupIncludingDiscontinuedOperationCurrent | 0 | 0 |

| + NotesAndLoansReceivableNetCurrent | 0 | 0 |

pacman::p_load(finreportr)

tesla_ann <- AnnualReports("TSLA")

tesla_ann

tesla_inc <- GetIncome("TSLA", 2018)

tesla_bs <- GetBalanceSheet("TSLA", 2018)

tesla_cf <- GetCashFlow("TSLA", 2018)

head(tesla_inc)But this code will not be able to access Tesla’s 2019 reports, because it throws an error:

edgar package

pacman::p_load(xml2, curl, edgar)

u1 <- "https://www.sec.gov/Archives/edgar/data/1318605/000156459020004475/tsla-10k_20191231_htm.xml"

url_file <- curl_download(u1, destfile = "~/Downloads/u1.xml") # to download and save

list_url_1 <- as_list(read_xml(u1)) # to read into R

cik.no <- 0001318605 # Tesla

form.type <- "10-K"

filing.year = 2019

quarter = c(1,2,3,4)

getFilings(

cik.no,

form.type,

filing.year,

quarter,

downl.permit = "y"

)NULLになりました。

Audit Staffing and Budgets

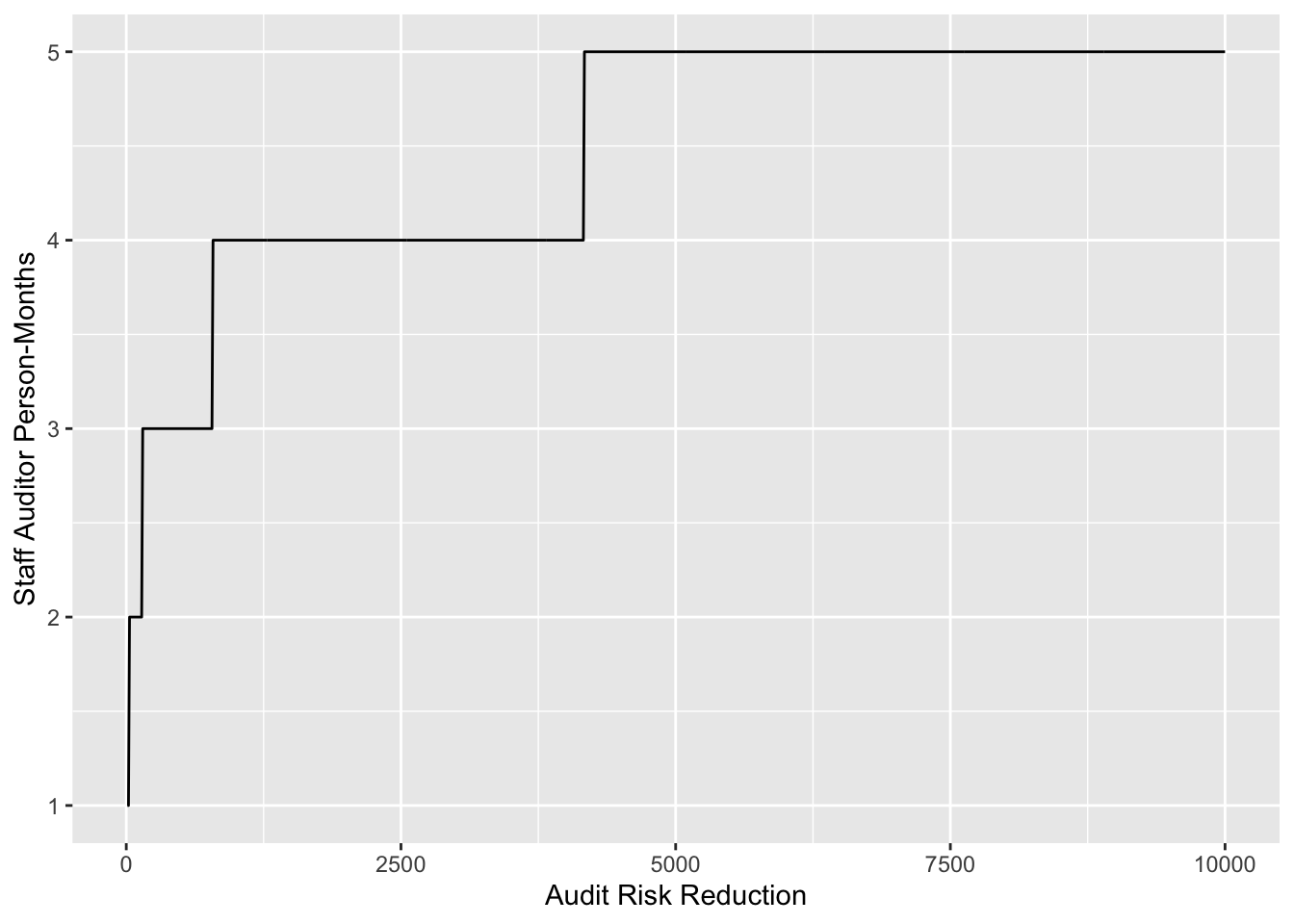

Audit Staffing and Budgets

benefit <- seq(10, 10000, 10) # 10から10000まで10刻み

staff_allocated <- data.frame(benefit, floor(10 * (log(benefit^.06))))

ggplot(staff_allocated, aes(staff_allocated[,1],staff_allocated[,2]) ) +

geom_line() + labs(x ="Audit Risk Reduction", y ="Staff Auditor Person-Months")

Shiny App

# Define UI for application

library(shiny) # Load the shiny package

ui <- fluidPage(

titlePanel("Risk Assessment Matrix"),

sidebarLayout(

sidebarPanel(

# Input: 監査テストの統計的信頼水準

sliderInput("confidence", "Confidence:",

min = .7,

max = .999,

value = .95),

# Input: サンプル取引ごとの監査コスト

sliderInput("cost", "Audit $ / transaction:",

min = 0,

max = 500,

value = 100),

# Input: Text for providing a caption for the RAM

textInput(

inputId = "caption",

label = "クライアント:",

value = "XYZ Corp.")

),

# Main panel for displaying outputs

mainPanel(

# Output: slider values entered

tableOutput("values"),

# Output: Formatted text for caption

h3(textOutput("caption", container = span)),

# Output: total cost of the audit

textOutput("view"),

# Output: RAM summary with sample sizes (scope) and cost

verbatimTextOutput("summary"),

h6("リスク選択: 1 = 低, 2 = 中, 3 = 高"),

h6("リスク知能 = ビジネス・インテリジェンス・スキャンニングで示されるリスク水準"),

h6("前年度リスク = 前期に監査人が示したリスク水準"),

h6("Scope = estimated discovery sample size that will be needed in the audit of this account"),

h6("Audit cost = audit labor dollars per sampled transaction"),

h6("Confidence = statistical confidence"),

h6("Account Amount and the Ave. Transaction size are in $ without decimals or 000 dividers")

)

)

)

# サーバー側の設定

server <- function(input, output) {

ram <- read.csv(system.file("extdata",

"risk_asst_matrix.csv",

package = "auditanalytics",

mustWork = TRUE)

)

sliderValues <- reactive({

data.frame(

Audit_Parameter = c("confidence", "cost"),

Value = as.character(c(input$confidence, input$cost)),

stringsAsFactors = FALSE)

})

output$values <- renderTable({

sliderValues()

})

output$caption <- renderText({

input$caption

})

output$summary <- renderPrint({

ram <- ram

conf <- input$confidence

cost <- input$cost

risk <- (10 - (as.numeric(ram[,2]) * as.numeric(ram[,3])) )/100

Scope <- ceiling( log(1-conf) / log( 1- risk))

ram <- cbind(ram[,1:5], Scope)

Min_cost <- Scope * cost

ram <- cbind(ram[,1:6], Min_cost)

ram

})

output$view <- renderText({ # 監査費用を表示

ram <- ram # リスク評価行列を読み込む

conf <- input$confidence # 監査の信頼度

cost <- input$cost # 監査費用

risk <- (10 - (as.numeric(ram[,2]) * as.numeric(ram[,3])) )/100 # リスク

Scope <- ceiling( log(1-conf) / log( 1- risk)) # 範囲

ram <- cbind(ram[,1:5], Scope) # リスク評価行列に範囲を追加

Min_cost <- Scope * cost # 最小監査費用を計算

minimum_audit_cost <- sum(Min_cost) # 最小監査費用を合計

c("Minimum estimated audit cost = ",minimum_audit_cost) # 最小監査費用を表示

})

}# Run the application

shinyApp(ui = ui, server = server)Generating the Audit Budget from the Risk Assessment Matrix

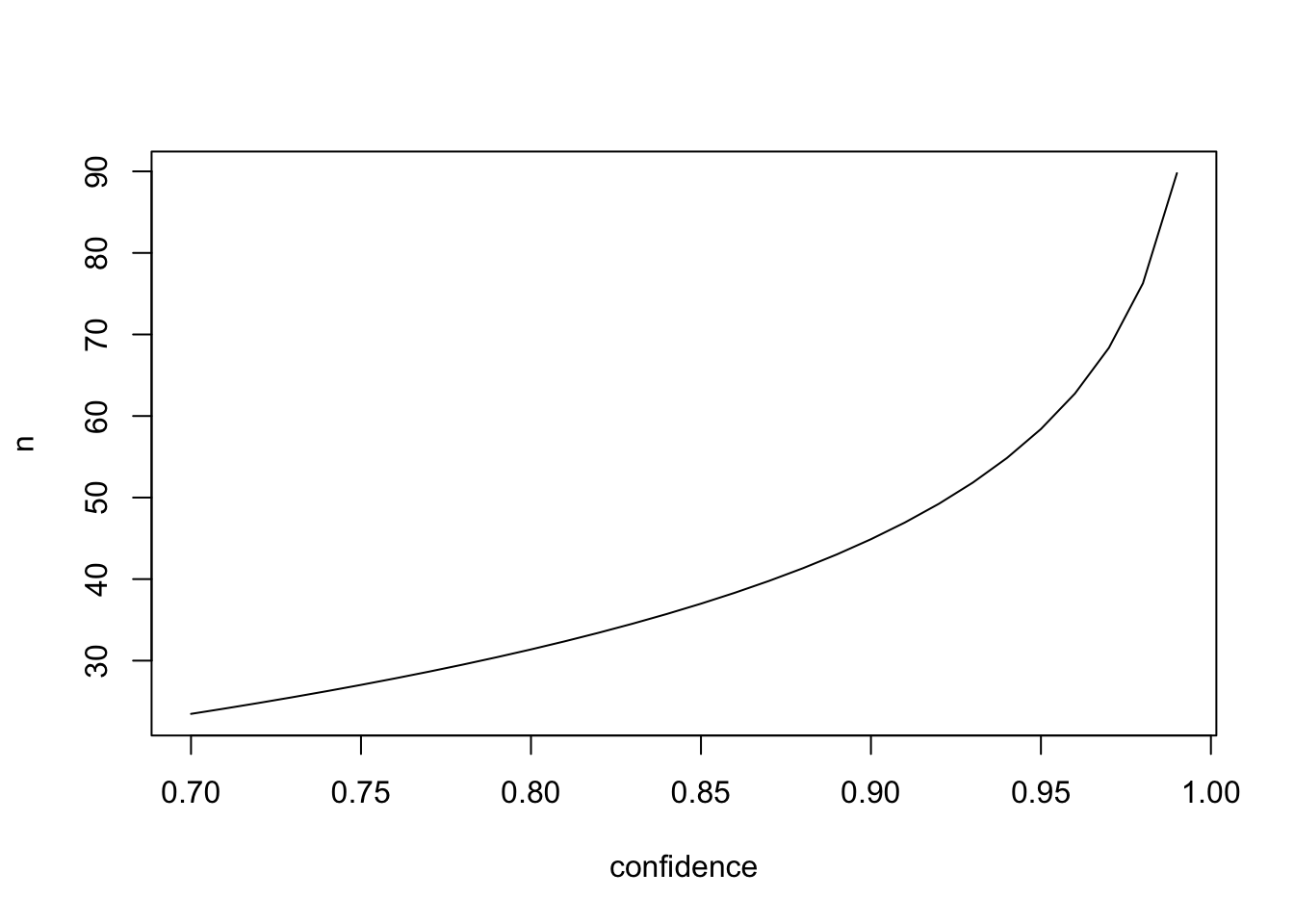

confidence <- seq(.99, 0.7, -0.01) # 0.99から0.7まで0.01刻みのベクトル

n <- (log(1 - confidence)) / log(1 - 0.05) # 発見サンプルサイズを計算

plot(confidence,n, type="l") # 発見サンプルサイズをプロット

confidence <- 0.95

n <- (log(1 - confidence)) / log(1 - 0.05)

cat("\n Discovery sample size = ", ceiling(n))

Discovery sample size = 59# install.packages("pwr") # first time only

library(pwr) # Cohen本のpower analysis

size <- 1000 # トランザクションの総数

Delta <- 0.05 * size # 5%の許容エラー率を検出する

sigma <- 0.3 * size # 変動(おそらく1/3)を推測する

effect <- Delta/sigma # 許容度÷変動

sample <- pwr.t.test( # pwr.t.test関数を使用

d = effect, sig.level = 0.05, power = 0.8,

type = "one.sample",

alternative = "greater" ## look for overstatement of earnings

)

cat("\n Attribute sample size for occurrence of error = ", ceiling(sample$n))

Attribute sample size for occurrence of error = 224size: 総トランザクション数(ここでは1000)。Delta: 許容エラー率として5%を想定しており、1000件中5%である「50件のエラーを検出できるようにしたい」という設定。sigma: 変動の範囲としてトランザクション数の約30%(1/3)を想定し、標準偏差に相当effect: 効果の大きさ(エラー率÷変動)で、これが実際に検出したい差を標準化したものd = effect: effectで計算された効果の大きさを指定。これは検出したいエラー率が、変動に対してどれだけの比率かを示しています。- sig.level = 0.05: 有意水準を5%に設定。

power = 0.8: 検出力(power)を80%に設定。これは、実際に効果が存在する場合にそれを80%の確率で検出できることを意味します。type = "one.sample": 1標本のt検定を使用する設定。つまり、1つの標本の平均が期待値と異なるかどうかを調べるもの。alternative = "greater": 片側検定で、「平均が期待よりも大きい」場合(例:利益の過大計上)を検出したいことを示しています。

size <- 100000 # 取引の総額

mu <- 50 # 取引の平均値

Delta <- 0.05 * mu # 5%の金額の許容誤差を検出

sigma <- 30 # 変動

effect <- Delta / sigma # 許容度÷変動

sample <- pwr.t.test( # Cohenのpower analysis

d = effect, # Cohenのd

sig.level = 0.05, # 有意水準

power = 0.8, # 効果量

type = "one.sample", # 一標本検定

alternative = "greater" # 偽陽性

)

cat("\n Attribute sample size for amount of error = ", ceiling(sample$n))

Attribute sample size for amount of error = 892